Personal loans are everywhere today.

A notification on your phone.

An ad promising instant approval.

A message saying you’re “pre-qualified”.

They’re positioned as quick, simple, and almost effortless.

And while personal loans are easier than most other forms of credit, they’re still a financial commitment, one that quietly shapes your monthly cash flow for years.

This blog isn’t here to rush you into taking a loan. And it isn’t here to warn you off either. It’s here to help you understand how personal loans actually work in real life, beyond ads, beyond EMI numbers, beyond approval messages. Because once you understand that, choosing the right personal loan becomes much easier.

How a Personal Loan Really Works?

At its core, a personal loan is straightforward. You borrow a fixed amount. You repay it in monthly instalments (EMIs). Each EMI has two parts:

- A portion that repays the loan

- A portion that pays interest

That’s it.

What complicates things isn’t the structure. It’s the choices made around the loan: interest rate, tenure, and how you approach repayment. Understanding those choices makes all the difference.

Secured vs Unsecured: Why Personal Loans Feel “Easy”

Personal loans are unsecured. That means you don’t need to offer:

- Property

- Gold

- A vehicle

This is why personal loans:

- Get approved faster

- Need less paperwork

- Feel more accessible

But there’s a trade-off. Because the lender doesn’t have security, they charge higher interest compared to secured loans. This doesn’t make personal loans bad. It simply means they’re made for convenience, not long-term borrowing. They work best when used thoughtfully.

Interest Rates: What You Should Pay Attention To

Most personal loans in India come with fixed interest rates.

This means:

- Your EMI stays the same every month

- Planning your budget becomes easier

But here’s something many borrowers don’t notice at first:

Even with a fixed EMI, interest is front-loaded. In the early months:

- A larger part of your EMI goes towards interest

- A smaller part reduces the loan amount

Over time, this balance slowly shifts. This matters because if you plan to close the loan early, or refinance later, timing affects how much interest you actually end up paying. Interest rate isn’t just a number. It’s a behaviour over time.

Simple vs compound interest

Personal loans usually follow a reducing balance method.

In simple terms:

- Interest is charged only on the remaining loan amount

- As you repay, interest reduces

This is borrower-friendly.

But here’s the part people overlook:

A small difference in interest rate may not change your EMI much, but it can significantly change the total amount you repay. Two loans can feel similar every month, yet cost very different amounts over their full tenure. That’s why comparing loans matters more than it seems.

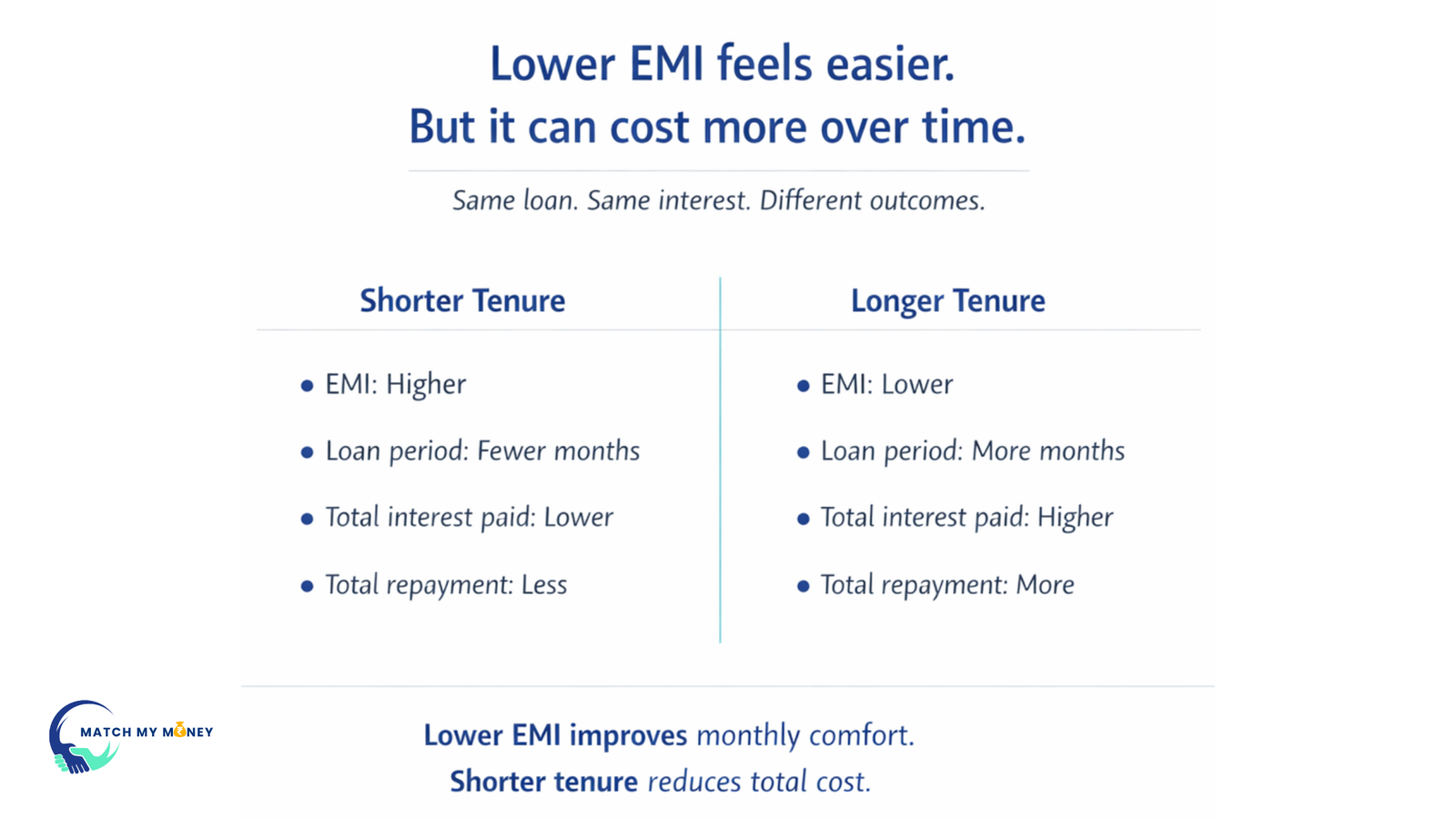

EMI: Why Lower Isn’t Always Better

Everyone looks at the EMI first. That’s natural. Lower EMI feels comfortable. It feels manageable. But comfort and smart borrowing aren’t always the same thing.

Your EMI depends on:

- Loan amount

- Interest rate

- Loan tenure

To reduce EMI, lenders often increase tenure. This works, but it also means:

- More months

- More interest

- Higher total repayment

A loan that feels easy today can quietly become expensive over time.

If personal loan terms ever feel confusing, this guide breaks them down simply.

Loan Tenure: Choosing What Fits Your Life, Not Just Your Budget

Personal loan tenures usually range from 12 to 60 months. Here’s how to think about tenure clearly:

- Shorter tenure → higher EMI, lower total interest

- Longer tenure → lower EMI, higher total interest

There’s no perfect number. The right tenure is one that:

- Doesn’t strain your monthly expenses

- Doesn’t stretch the loan unnecessarily

A good rule: Choose the shortest tenure you can comfortably manage, not the longest one offered.

Is Taking a Personal Loan a Good Idea?

Yes, when used with clarity.

A personal loan can make sense if:

- You need funds urgently

- You have predictable income

- You know how you’ll repay it

It becomes a problem when:

- It’s taken casually

- It’s used repeatedly to cover lifestyle gaps

- One loan leads to another

A personal loan is just a tool. How you use it determines whether it helps or hurts.

What About Credit Score?

Handled well, personal loans can help build credit.

Paying EMIs on time:

- Improves repayment history

- Shows credit discipline

- Strengthens your profile

But there’s one thing to be careful about. Applying across multiple apps or websites can lead to too many credit enquiries in a short period. That can work against you.

Smart borrowers:

Why Comparison Matters More Than Speed

Two personal loan offers can look very similar at first glance:

- Same loan amount

- Similar EMI

- Same tenure

But differ in:

- Interest rate

- Processing fees

- Prepayment or foreclosure terms

- Total repayment

Without comparison, these differences stay hidden. And once you’ve taken the loan, changing it isn’t always easy. That’s why a little patience before applying often saves money later.

Here’s a simple guide on how to compare personal loan offers properly, without getting overwhelmed.

How to Think About Personal Loans Before Applying

Instead of asking: “How fast will I get the money?”

Also ask:

- How much will I repay in total?

- How flexible is the loan if my situation changes?

- Does this loan fit my income, not just my eligibility?

When you think this way, borrowing becomes intentional, not reactive. If you want to go deeper, here are some common personal loan mistakes people make and how to avoid them.

Where Match My Money Comes In

Once you understand how personal loans work, the next step is simple: comparison. Match My Money exists to make that step easier. Instead of jumping between apps or guessing which loan is right, Match My Money lets you:

- Compare personal loan options in one place

- See interest rates, tenure, and key charges clearly

- Choose a loan that fits your situation, not just one that approves quickly

A Final Thought Before You Decide

Personal loans aren’t dangerous. And they’re not magical solutions either. They work best when you understand them and choose them consciously. If you’re planning to take a personal loan, pause for a moment.

Read once.

Compare calmly.

When you’re ready, Match My Money helps you find a personal loan that actually fits.