This happens every year to salaried employees. It’s not random.

If your take-home salary drops in January, February, or March, it usually has nothing to do with your job or performance.

-Your role didn’t change.

-Your CTC didn’t change.

-Your income didn’t suddenly fall.

Yet the amount credited to your bank account is noticeably lower.

This happens to a large number of salaried employees every year. Most people assume:

- HR made a mistake

- TDS is being deducted “randomly”

- something went wrong with payroll

In most cases, none of that is true. What you’re seeing is the tax system catching up late in the financial year.

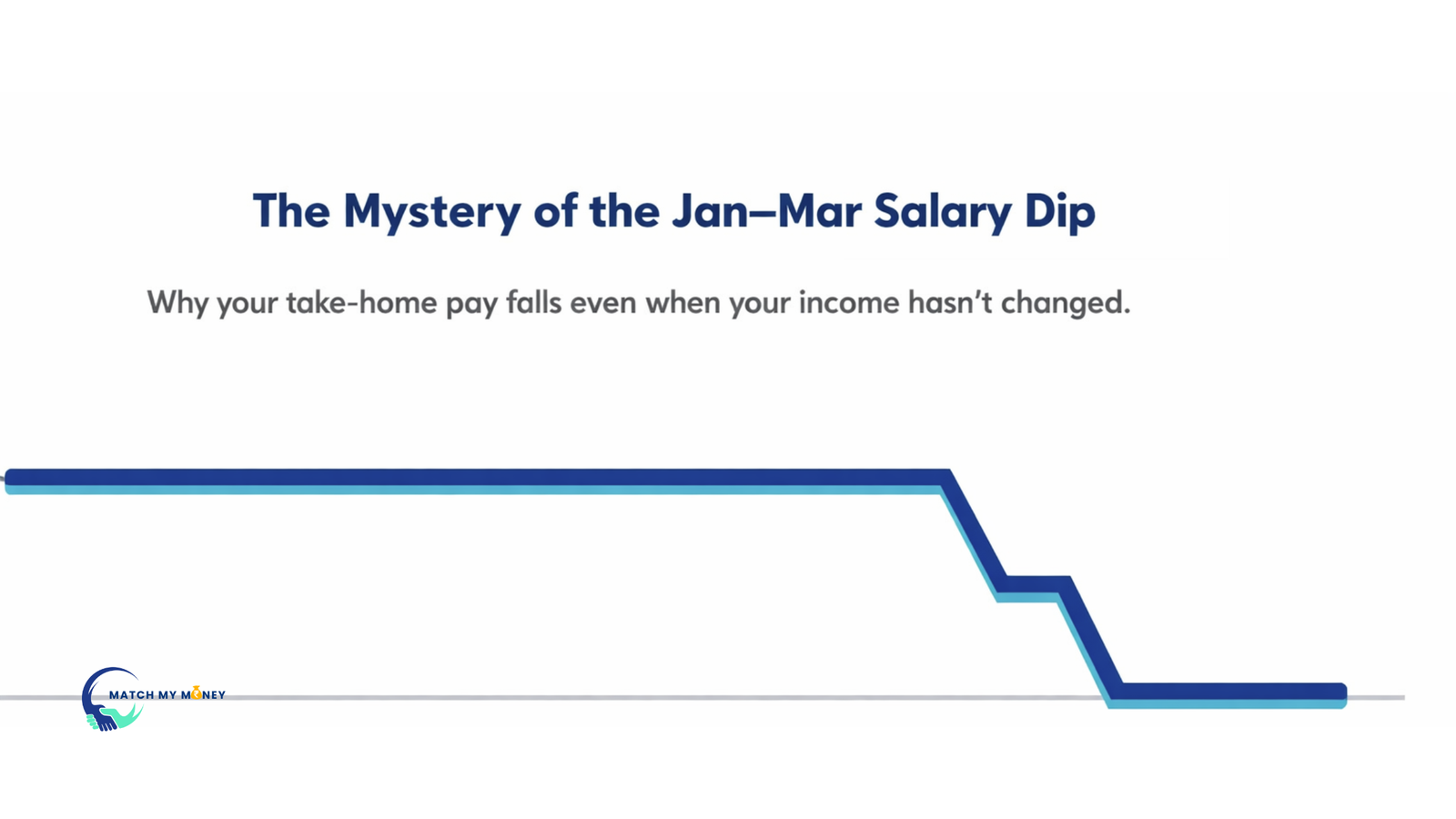

January–March salary pressure is rarely a spending problem. It’s a timing problem.

Tax decisions that were delayed, assumed, or left incomplete earlier in the year get reconciled in the last quarter and the correction is compressed into just a few months. That’s why the drop feels sudden and sharp.

This guide explains why this happens, what makes the drop worse, what still helps once you’re already in Jan–Mar, and how to make sure it doesn’t repeat next year.

What Actually Happens Behind the Scenes (And Why the Hit Comes Late)

To understand why your salary drops in January–March, you need to understand how payroll handles tax in practice, not how tax is explained in theory.

Most people assume TDS is calculated month by month. It isn’t.

How TDS Actually Works for Salaried Employees

Your employer doesn’t calculate tax independently each month. Instead, payroll works like this:

- Your total annual income is estimated

- Your total tax liability for the year is calculated

- That tax is then spread across the remaining months as fixed TDS

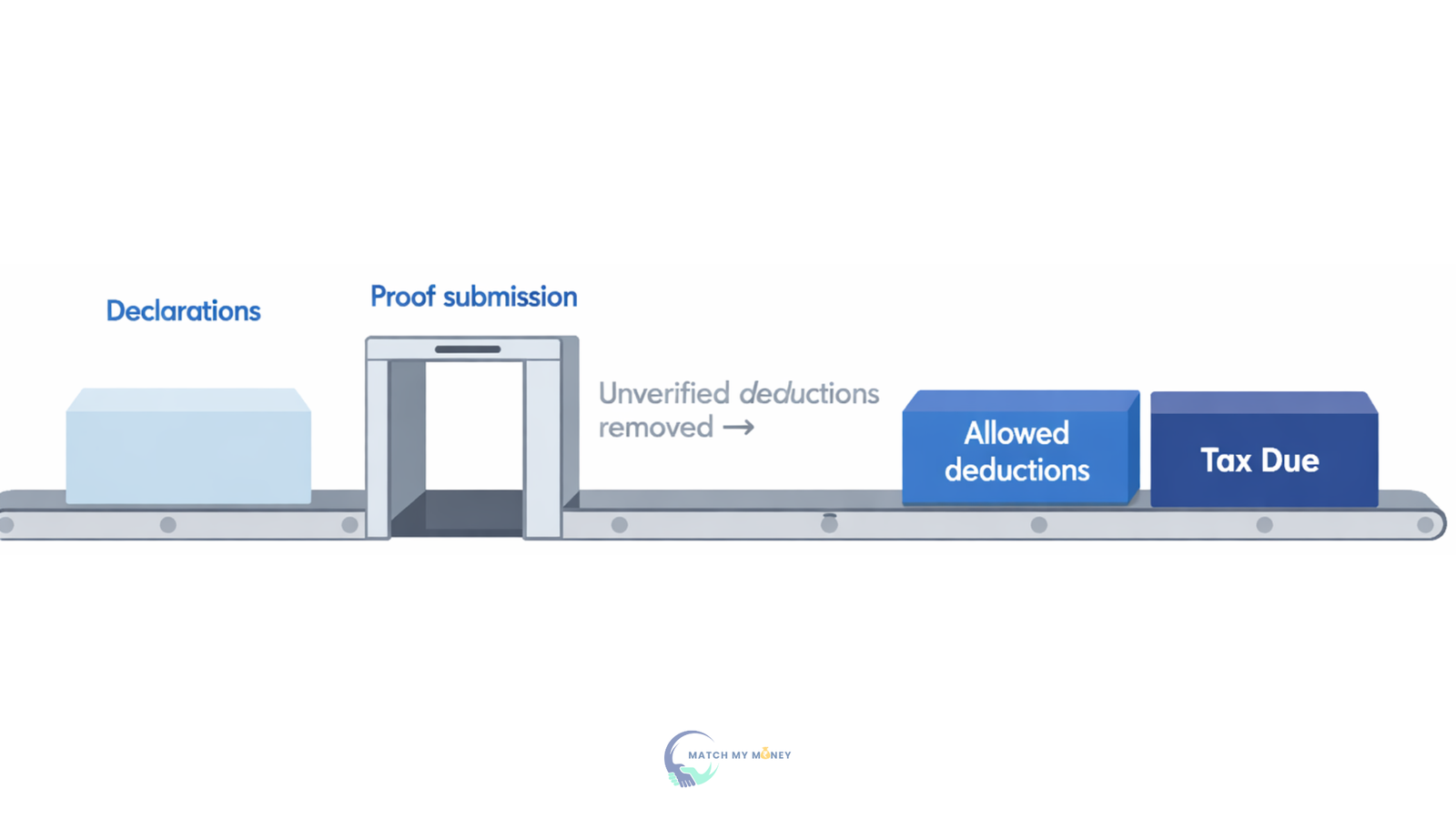

This system depends entirely on the information available at that point in time, especially your declared deductions.

Why April to December Feels Stable

In the first three quarters of the year, payroll operates on trust and projections.

From April to December:

- Declared deductions are assumed to materialise

- Investment plans are treated as future commitments

- Proofs are expected later

Because of this, monthly TDS stays relatively smooth, even if nothing has actually been executed yet. This creates a false sense of stability.

What Changes in January

January is when assumptions stop.

At this stage:

- Proof submission deadlines approach

- HR begins verifying what actually exists

- Deductions that weren’t executed are removed

When deductions disappear, taxable income increases. But the annual tax liability doesn’t change. So payroll has only January, February, and March left to recover the gap.

Why the Drop Feels Sudden

The system doesn’t soften or stagger the correction. If you underpaid tax earlier because deductions were assumed but didn’t materialise, the remaining tax is simply compressed into fewer months.

That’s why:

- TDS jumps sharply

- Take-home salary drops

- The change feels abrupt

Nothing new happened in January. The system just caught up.

Why HR Can’t “Fix” This Late in the Year

Once year-end reconciliation begins:

- Payroll can’t spread tax backward

- Deductions can’t be assumed without proof

- Statutory TDS can’t be reduced arbitrarily

At this stage, payroll is correcting a shortfall, not making a new decision.

The One Insight That Matters

January–March salary pressure isn’t punishment. It’s reconciliation.

It’s what happens when:

- planning is delayed

- assumptions don’t match reality

- and the system runs out of time

Once you understand this, the stress becomes easier to handle and far easier to prevent next year.

The Triggers That Make the Jan–Mar Salary Drop Worse

Not everyone sees the same salary drop between January and March. For some, it is manageable. For others, it feels sudden and severe.

The difference usually comes down to a few specific triggers. If even one of these applies to you, the year-end correction tends to be sharper.

1. Declared Investments That Were Never Executed

This is the most common trigger.

Early in the year, many employees declare deductions they intend to act on later, such as ELSS investments, insurance premiums, or PPF contributions.

Payroll treats these declarations as commitments. When they are not executed, the deductions are removed during verification in January.

That immediately increases taxable income. The tax itself was always due, but now it has to be recovered in fewer months.

This does not mean you lost money in January. It means tax that was postponed earlier was collected late.

2. Tax Regime Chosen Without Recalculation

Many salaried employees repeat last year’s tax regime or choose the new regime because it feels simpler.

The problem is that salaries, rent, insurance, and deductions change year to year. A regime that worked earlier may no longer be optimal.

When payroll reconciles the actual numbers near year-end, the mismatch shows up as higher TDS in the final months.

A wrong regime choice rarely hurts immediately. It hurts when there is no time left to adjust.

3. HRA Claimed but Not Fully Valid

Paying rent alone does not guarantee HRA exemption.

Issues arise when rent receipts are missing, landlord PAN is not provided where required, the salary structure does not include HRA, or the rent paid does not support the exemption claimed.

HRA is often one of the largest deductions. When it is reduced or disallowed during verification, the tax impact shows up late and feels disproportionate.

4. Insurance Deductions Planned but Not Paid

Health insurance deductions under Section 80D are often assumed early in the year.

If premiums are not actually paid before proof submission, the deduction does not exist. When it drops off in January, payroll adjusts tax immediately.

This is another case where intention was treated as execution until verification forced a correction.

5. Variable Income Accounted for Late

Bonuses, incentives, and performance pay are often paid toward the end of the year.

If variable income was not included accurately in earlier tax estimates, payroll adjusts sharply once the final income becomes clear.

The tax on variable pay is not unexpected. The timing of its recovery is what creates pressure.

6. Pushing All Decisions to Year End

This is less about a single mistake and more about a pattern.

When tax decisions are pushed to January or February, there is no runway left for gradual correction.

Payroll systems are built to reward early clarity. Late clarity leads to compression.

What Actually Helps When You’re Already in Jan–Mar

Once January hits and your take-home salary has already dropped, much of the advice you’ll find online stops being useful.

Suggestions like “start investing early next year” or “plan better” may be true, but they do nothing for the current situation.

So it helps to be clear about what is no longer possible, what still works, and what usually makes things worse.

What You Can’t Change at This Stage

Once payroll enters year-end reconciliation, you typically cannot:

- reverse TDS already deducted

- spread tax across earlier months

- claim deductions that were never executed

- change how past payroll calculations were done

At this point, the system is correcting a shortfall, not planning ahead. Accepting this early prevents rushed decisions that create new problems.

What Still Helps and Is Worth Checking

1. Execute Only Deductions That Were Already Planned and Are Still Valid

Some deductions remain valid if completed before March 31, such as health insurance premiums, certain eligible 80C investments, or delayed home loan interest certificates.

Only act if:

- the payment was already part of your plan

- you can complete it immediately

- proof can be submitted within payroll deadlines

Do not make new investments solely to reduce tax if they strain cash flow or lock money unnecessarily.

2. Verify That Payroll Has Counted Everything Correctly

Late in the year, genuine errors do happen. Confirm that:

- PF deductions are reflected accurately

- HRA exemption is applied correctly

- variable pay is not double-counted

- insurance premiums already paid are included

If something legitimate is missing, raise it with HR or payroll immediately. This will not undo the correction, but it can prevent excess deduction.

3. Adjust Cash Flow, Not Core Commitments

A sudden drop in salary often triggers the wrong response.

Cutting essentials, delaying EMIs, or questioning long-term affordability usually isn’t necessary. This is a short-term compression, not a permanent income issue.

Focus instead on:

- postponing discretionary spending

- using short-term buffers

- keeping fixed commitments stable

The goal is to absorb a timing hit, not to redesign your financial life.

What Usually Makes Things Worse

Avoid:

- making financial decisions out of panic

- borrowing without understanding total cost

- buying tax products you do not fully understand

- assuming this pattern will repeat every year

Most January–March salary pressure is situational. Treating it like a structural problem often causes more damage than the tax adjustment itself.

When a Short-Term Personal Loan Can Make Sense

In some cases, year-end tax correction creates genuine short-term pressure. Expenses remain fixed while take-home salary drops temporarily.

A short-term personal loan can make sense only if:

- the pressure is clearly limited to Jan–Mar

- your income remains stable

- the loan is used as a bridge, not a habit

- you have a clear repayment plan once the financial year resets

It should not be used to fix tax mistakes, fund lifestyle spending, or roll balances month after month.

Borrowing does not solve tax planning issues. At best, it smooths timing gaps, and only when used carefully.

If you explore this option, prioritise short tenures, transparent pricing, and lenders that clearly disclose total repayment, not just EMI. Platforms like Match My Money help compare such options transparently so borrowing, if needed, remains controlled and predictable.

How to Make Sure This Doesn’t Happen Again Next Year

January–March salary pressure feels harsh mainly because it arrives late and without warning. The reason it’s so stressful is also why it’s easy to prevent.

1. Decide Your Tax Regime at the Start of the Year

The tax regime decision is often treated as a year-end task. That’s where problems begin Instead, recalculate your regime choice in April using what already exists:

- current salary structure

- rent and HRA eligibility

- PF contributions

- insurance premiums

- EMIs, if any

Once the right regime is chosen early, payroll can spread tax evenly across the year. There is very little left to correct later.

Choosing the wrong tax regime early in the year is one of the biggest reasons TDS corrections pile up at year-end. If you’re unsure which option suits your current salary, deductions, and rent, this detailed guide explains how salaried employees should choose between the old vs new tax regime for salaried employees.

2. Declare Only What Is Already in Motion

This single habit prevents most year-end shocks. When submitting declarations:

- declare deductions that are already executed or recurring

- avoid entries based on future intent

- treat declarations as commitments, not placeholders

Payroll systems trust your declaration. Issues arise only when execution does not match what was declared.

3. Assume Variable Pay Is Taxable From Day One

Bonuses and incentives should never be treated as unexpected income. If your compensation includes variable pay:

- assume it is taxable

- expect higher TDS in the months it is paid

- plan cash flow accordingly

This mindset prevents surprise deductions when variable income shows up later in the year.

4. Design a Small Buffer for Year-End Adjustment

You do not need a large emergency fund specifically for tax.

A buffer equal to one slightly lower take-home month is usually enough to absorb year-end corrections calmly.

This is not about saving more. It is about designing for a known timing issue.

5. Revisit Your Setup Once Every Year

Life changes. Your tax setup should reflect that.

Marriage, rent changes, insurance additions, home loans, or income jumps can all change what works best.

Reviewing your tax choices once a year is not overthinking. It is basic maintenance.

The Bottom Line

A January–March drop in take-home salary is rarely a sign of poor money management. It’s what happens when delayed decisions meet a system that settles accounts on a fixed timeline.

Nothing broke in January. Nothing suddenly changed. Tax that was always due was simply collected late.

Once you understand this, the experience stops feeling personal and starts feeling predictable.

The only real variable is timing. When tax choices are made early and declarations reflect what already exists, there is nothing left for payroll to correct at the end of the year.

Handled this way, January to March becomes uneventful. And uneventful is exactly how your salary should feel.