What Is a Loan Comparison Platform & How Does It Work?

What Is a Loan Comparison Platform and How Does It Work? Your salary gets credited at the start of the month. A few days later,

Your salary gets credited at the start of the month. A few days later, the bills, EMIs, and unexpected expenses start piling up. Sometimes, even the best budgeting can’t cover it all. That’s when many people turn to personal loans.

But here’s the catch: one bank might offer you a loan at 10.5%, another at 13%, and a fintech app might approve instantly but with higher processing fees. With so many choices, how do you know which one is actually best for you?

That’s exactly the problem a loan comparison platform solves.

If you are specifically looking for tips on selecting the right personal loan, check our guide on how to choose the best personal loan in India.

A loan comparison platform is a digital marketplace that allows borrowers to view, compare, and apply for loans offered by multiple banks, NBFCs, and fintech lenders. Instead of visiting ten different websites or branches, you fill in your details once and get a clear view of all the available loan options.

Think of it as the MakeMyTrip of loans, but instead of flights, you compare interest rates, processing fees, loan tenures, and eligibility criteria.

India’s salaried workforce, especially in the Tier-1 cities is increasingly credit-reliant. Whether it’s managing wedding expenses, paying for higher education, funding a home renovation, or handling unexpected medical costs, personal loans have become a go-to solution.

According to IMARC Group, the India personal loan market was valued at USD 135.7 billion in 2024 and is projected to reach USD 556.3 billion by 2033, reflecting a compound annual growth rate (CAGR) of 15.70% during 2025–2033.

In such a competitive lending environment, comparison platforms empower borrowers to make informed, confident decisions.

The choice of lender also matters. Read our comparison of banks vs. NBFCs for personal loans to understand which suits your needs better.

The process is simple, but behind the scenes, it’s powered by technology, partnerships, and strict compliance. Here’s how it works:

Typically, platforms ask for your name, age, income, employment type, city, and existing obligations like EMIs.

The platform checks your profile against lender criteria. For example, if your salary is ₹50,000 a month, some lenders might pre-qualify you for loans up to ₹10 lakh.

You see a list of loan options with details such as:

Instead of juggling spreadsheets, you get side-by-side comparisons. Some platforms even offer EMI calculators to check affordability.

Once you pick an offer, the platform either redirects you to the lender’s site or completes the application on your behalf. Lenders then run credit checks, usually via your CIBIL score.

On approval, the loan amount is disbursed directly to your bank account, sometimes within 24–48 hours.

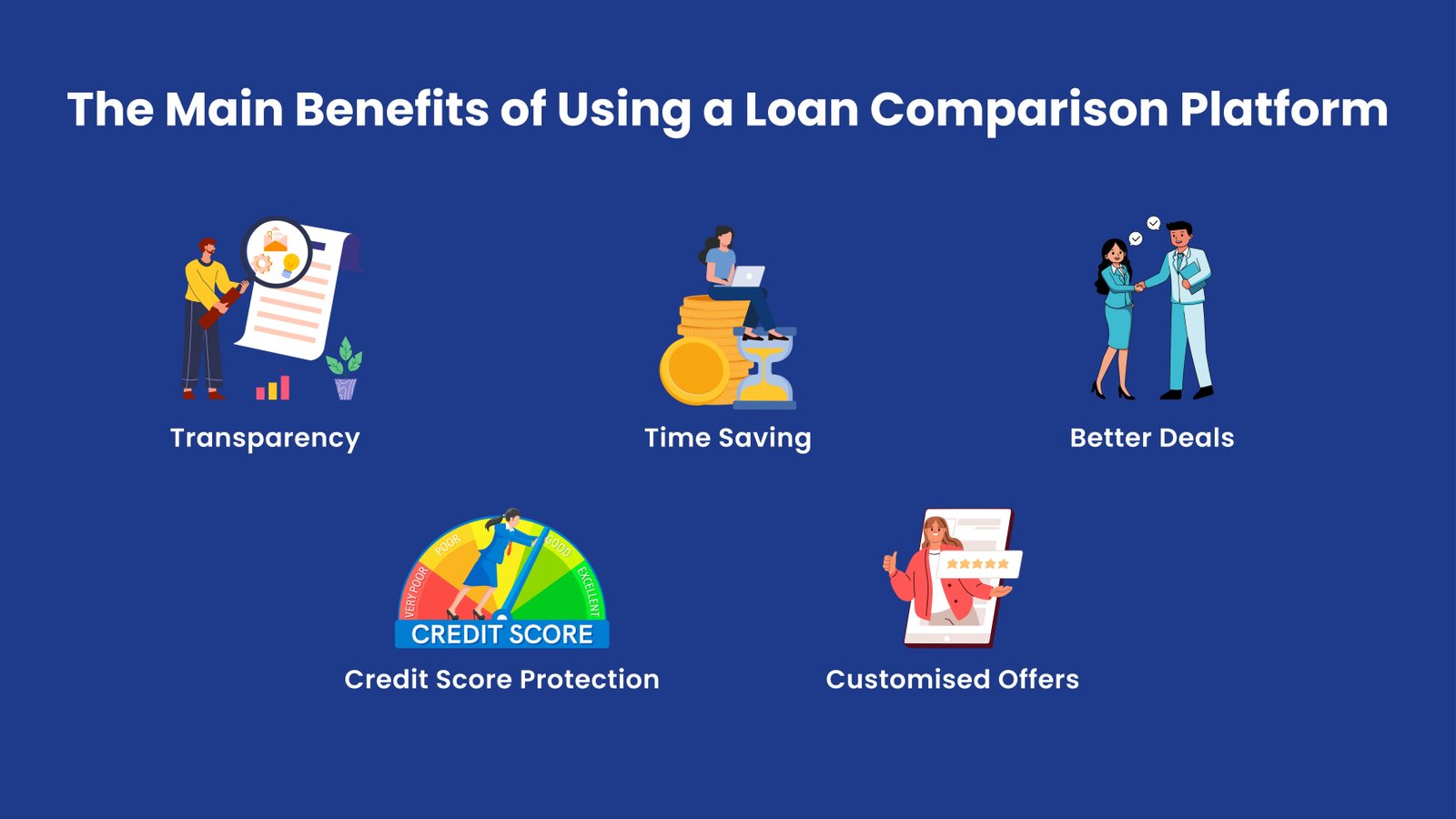

For salaried individuals in India, the value of a loan comparison platform lies in making borrowing simpler, faster and smarter. Here’s how:

Instead of being lured by ads that say “lowest rate starting from 9%”, you see the actual rate you qualify for along with fees and EMI details. This clarity helps you avoid surprises later.

Example: If Bank A offers you 11.2% with a ₹1,000 processing fee and Bank B offers 10.9% but with a ₹5,000 fee, the platform shows you the real cost so you don’t get misled by just the headline rate.

Normally, applying to multiple lenders means filling forms again and again, submitting salary slips separately and waiting for each bank to respond. A comparison platform cuts through this. One form gives you access to multiple offers instantly.

Tip: If you’re planning for something time-sensitive such as wedding expenses or medical bills, this feature can save you days of effort.

Because platforms bring lenders together, the competition often works in your favour. Lenders know you’re comparing, so many offer preferential rates or faster approvals through these platforms.

Did you know some banks and NBFCs run exclusive promotional rates only on aggregator platforms to attract borrowers.

Each time you apply directly with a bank, they may pull a “hard enquiry” on your credit report, which can bring down your CIBIL score. Platforms usually start with a soft check to pre-qualify you. This way, you can compare options without hurting your score.

Why this matters: If you plan to take a home loan or car loan in the future, protecting your credit score today ensures better eligibility tomorrow.

Your salary, employer and repayment history influence your loan eligibility. A good platform uses these inputs to filter out irrelevant options and only show lenders where you stand a strong chance of approval.

For example: If you work in a reputed MNC, some lenders may offer you lower rates or higher limits. The platform highlights these benefits automatically.

The bottom line: Using a loan comparison platform is not just about saving money. It is about making sure you choose a loan that truly fits your financial situation without hidden stress later.

A loan comparison platform makes the process easier, but the final choice is still yours. To avoid paying more than you should, pay attention to the following points:

Do not just focus on the advertised interest rate. Check the Annual Percentage Rate (APR), which includes processing fees, insurance, documentation costs and other charges. APR gives you the true cost of the loan.

Some lenders charge up to 3% for processing your loan, while others may add penalties if you repay early. If you plan to clear your loan before the full term, these costs can affect your savings.

The length of your loan term matters. A longer tenure reduces the monthly EMI but increases the total interest you pay over time. A shorter tenure means higher EMIs but quicker debt freedom. Use the EMI calculator on the platform to balance affordability and cost.

Always read the fine print. Look out for terms on partial pre-payment, foreclosure rules and late payment charges. Even small penalties can add up over the life of a loan.

Make sure the lender reports timely repayments to credit bureaus. This helps build your CIBIL score, improving your chances of getting bigger loans in the future at lower interest rates.

While not always listed in the offer, the quality of a lender’s support matters. Quick resolution of queries, transparent communication and smooth digital processes can make your borrowing experience more reliable.

The lending market in India is changing quickly, and loan comparison platforms are adapting to meet new borrower needs. Here are some of the key trends:

A growing majority of salaried individuals now prefer to apply for loans online. In fact, over 70% of personal loan applications are now initiated digitally. This shows that borrowers are comfortable with digital platforms and trust them to handle important financial decisions.

Loan comparison is no longer limited to large personal loans. Platforms are beginning to showcase Buy Now Pay Later (BNPL) and smaller ticket-size loans, giving users more flexibility for short-term or everyday expenses.

Some platforms are adding features that help borrowers track and improve their CIBIL score. This is important because a better score can unlock access to larger loans at lower interest rates in the future.

While the early growth came from big metros, more salaried professionals in smaller cities are now using these platforms. Cities like Jaipur and Lucknow are seeing strong adoption, which shows that the shift towards digital borrowing is spreading nationwide.

Do I need to pay any charges to use a loan comparison platform?

No, borrowers do not pay any fee. These platforms earn their commission directly from banks and NBFCs, so you can use them free of cost.

Is my salary enough to qualify for a personal loan?

Most lenders require a minimum net monthly salary, often around ₹15,000–₹25,000 depending on the city and employer. The higher your income and the more stable your job, the better your chances of approval.

Will checking multiple offers hurt my credit score?

No, simply comparing offers does not affect your CIBIL score. Your score is only impacted when a lender makes a “hard enquiry” during the final application stage.

How quickly will the loan be disbursed?

Once approved, many lenders disburse personal loans within 24–48 hours. Some fintech lenders even process the amount on the same day.

Are there any tax benefits on personal loans?

There are no general tax benefits on personal loans. However, if the loan is used for specific purposes like home renovation or education, you may be eligible for certain deductions under Indian tax laws.

What happens if I miss an EMI?

Missing EMIs can attract late fees and may lower your credit score. It is best to set up auto-debit from your salary account to avoid missing payments.

For many salaried professionals, personal loans are a practical way to handle urgent or planned expenses. But choosing the wrong lender can mean higher EMIs, unnecessary charges and long repayment stress.

A loan comparison platform takes the uncertainty out of borrowing. It helps you compare real offers side by side, understand the true cost of credit and select a loan that matches your salary and repayment comfort.

The smart choice is simple: compare first, apply later, and borrow with confidence.

What Is a Loan Comparison Platform and How Does It Work? Your salary gets credited at the start of the month. A few days later,