Figuring out how to compare personal loan offers can feel like a maze.

You open one app, it says Instant approval at 10.99%.

Another claims, Lowest rate guaranteed.

And somehow, after 20 minutes of scrolling, you’re even more confused.

Many working professionals go through this, trying to make sense of endless offers that all sound the same.

A recent RBI Financial Stability Report noted that personal loans grew over 30% year-on-year, driven mostly by salaried professionals seeking short-term credit, yet most borrowers compare offers only on interest rate, missing hidden costs and flexibility.

With every lender claiming to be the fastest or cheapest, knowing who to trust becomes the hardest part.

This blog breaks it all down simply, showing you how to compare personal loan offers like a pro, so you can borrow smart, avoid hidden traps, and choose what truly fits your needs.

Also read: How to Choose the Best Personal Loan in India, to understand what affects your loan rates in the first place.

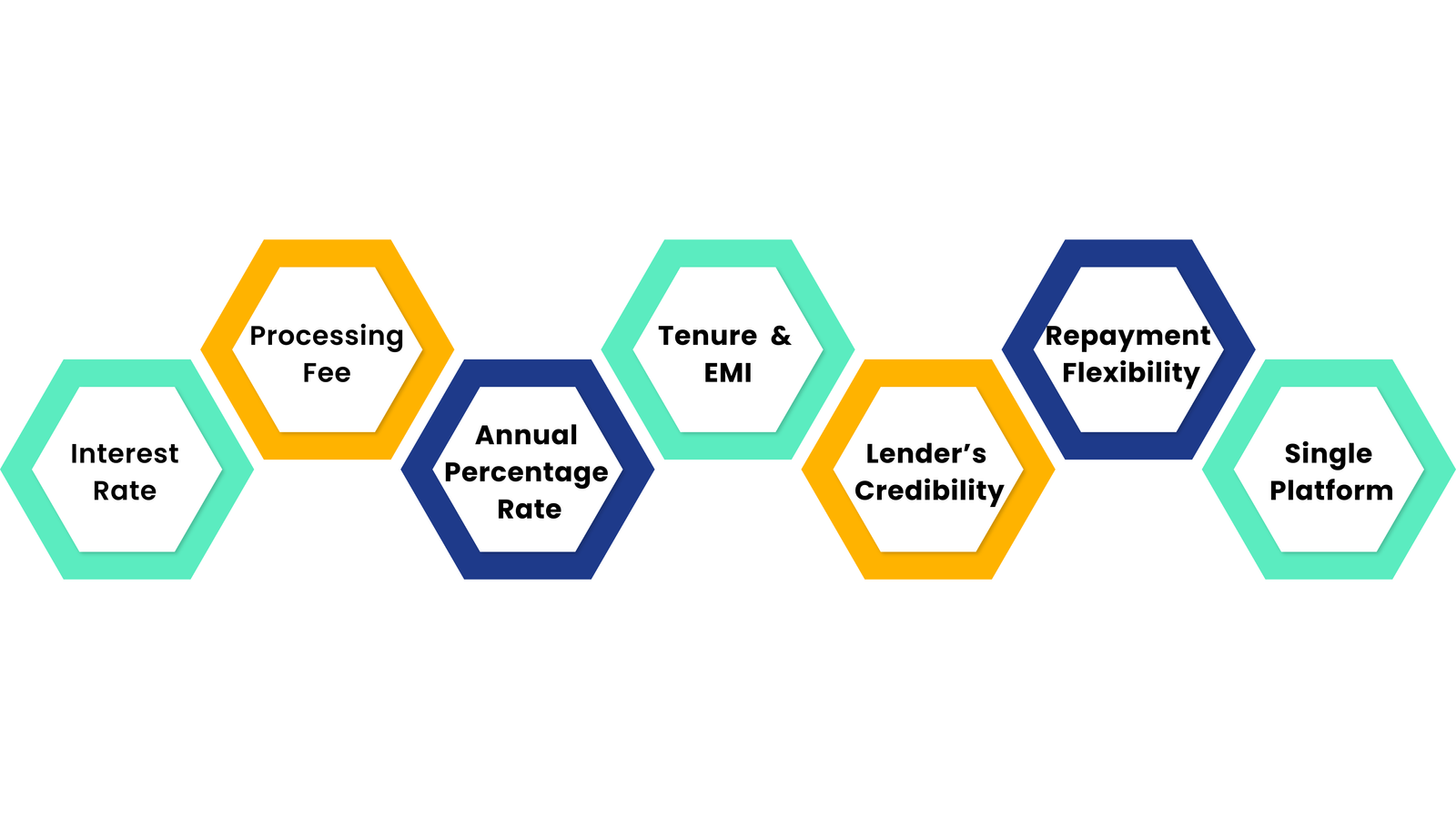

Main Factors to Check Before You Compare Personal Loan Offers

Before you apply anywhere, it helps to know what really matters. Whether it is interest rates, fees, tenure or lender credibility. Here’s where to start:

1. Start With the Interest Rate, But Don’t Stop There

When you compare personal loan offers, the interest rate is usually the first thing that catches your eye.

And yes, it matters, but it’s not the only number that decides what you’ll actually end up paying.

Two loans can both claim “10% interest,” yet one can cost you thousands more depending on how that interest is calculated.

Flat vs. Reducing Balance Rate (Know the Difference)

| Type of Interest | What It Means | Example |

| Flat Rate | Interest is charged on the entire loan amount for the full tenure. | ₹1 lakh @ 10% flat → ₹10,000 interest per year, even as you repay. |

| Reducing Balance Rate | Interest is charged only on the outstanding amount after each EMI. | ₹1 lakh @ 10% reducing → roughly ₹5,500 interest per year. |

Pro Tip

Always ask if your loan rate is flat or reducing balance. A reducing rate might look higher, but it’s usually cheaper in the long run.

Why Is This Important?

If you’re comparing offers from different lenders, check the type of rate before assuming one is better. For example, some smaller NBFCs or instant-loan apps may highlight a flat rate to appear competitive, but your actual cost of borrowing can be 20–30% higher.

According to RBI data (2024), personal loan interest rates in India range from 10.25% to 24%, depending on your credit score, employer profile, and income bracket.

That’s why understanding how interest is applied is the first real step in learning how to compare personal loan offers effectively.

2. Compare Processing Fees and Hidden Charges

When you compare personal loan offers, don’t stop at the interest rate, because a cheaper rate can still become an expensive loan once you add all the extra charges.

These fees often slip past unnoticed during application but show up later in your repayment plan. Understanding them upfront helps you compare loans fairly and avoid surprises.

Common Loan Charges You Should Know

| Charge Type | Typical Range | What It Really Means |

| Processing Fee | 1% – 3% of the sanctioned loan amount | Deducted before disbursal. Ask if it’s refundable on rejection or partially waived during offers. |

| Prepayment / Foreclosure Fee | 2% – 5% of the remaining balance | Charged if you clear your loan early. The best lenders cap this at 0–2%. |

| Late Payment Fee | ₹500 – ₹1,000 or 2% of EMI | Added automatically to your next EMI — usually hidden in the fine print. |

| Part-Payment Fee | 1% – 3% of prepaid amount | Some lenders restrict the number of part-payments allowed per year. |

💡 Pro Tip: Always check the loan agreement summary or Most Important Terms & Conditions (MITC) sheet before signing. RBI guidelines require lenders to list all charges clearly — but not every app highlights them upfront.

How Major Banks and NBFCs Compare on Fees

[Source: HDFC Bank & ICICI Bank Personal Loan Pages, Nov 2025] |

Why These Costs Matter

Let’s say you borrow ₹2 lakh for 2 years at 11% interest.

If Lender A charges a 3% processing fee and Lender B charges 1%, the difference in upfront cost alone is ₹4,000, before you even start repayment.

That’s why comparing fees side-by-side is as important as comparing rates.

Related Read

What Is a Loan Comparison Platform

Learn how platforms like Match My Money display all-inclusive APRs (interest + fees) from multiple RBI-registered lenders, so you know the true cost before applying.

3. The Number That Matters More Than Interest Rate: Your APR

Most people think comparing interest rates is enough. But that number only tells part of the story.

The real cost of your loan depends on the Annual Percentage Rate (APR), a figure that combines interest rate, processing fees, and other charges into one all-inclusive number.

What APR Really Means

| Term | What It Includes | Why It Matters |

| Interest Rate | The base cost of borrowing money | What lenders advertise most prominently |

| Processing Fees & Charges | One-time costs added at the time of approval | Can increase the total cost significantly |

| APR (Annual Percentage Rate) | The true yearly cost including all fees | Shows what you’ll actually pay over time |

Let’s say you’re borrowing ₹2,00,000 for 2 years:

| Lender | Interest Rate | Processing Fee | Total Cost (Approx.) | Which Is Cheaper? |

| Lender A | 10.5% | 3% | ₹2,23,000 | ❌ Looks cheaper but isn’t |

| Lender B | 11.5% | 1% | ₹2,21,000 | ✅ Slightly higher rate, lower cost overall |

Even though Lender B has a higher “interest rate,” the effective APR is lower, meaning you actually pay less.

Pro Tip

As per RBI’s Fair Practices Code, lenders must now disclose an all-inclusive APR before disbursal. If an app or NBFC doesn’t, that’s a red flag, it may be hiding extra costs.

Source: RBI Circular on Fair Lending Practices, 2023

Why Knowing Your APR Makes a Big Difference

- It helps you compare apples to apples across different lenders.

- It protects you from “low-rate” traps with high upfront fees.

- It’s especially useful for short-term loans where charges form a big portion of total cost.

4. Choose the Right Tenure and EMI: Balance Comfort and Cost

When comparing personal loan offers, tenure is often the deciding factor between a comfortable EMI and an expensive loan.

Most people just pick the option with the smallest EMI, but that can cost much more in the long run.

How Tenure Changes the Real Cost

| Example: ₹2,00,000 loan @ 12% interest | 2 Years | 5 Years |

| Monthly EMI | ₹9,415 | ₹4,449 |

| Total Interest Paid | ₹26,000 | ₹67,000 |

A longer tenure reduces your monthly burden but increases the total interest you pay.

A shorter tenure saves money overall but demands higher monthly cash flow.

What’s the Ideal EMI-to-Income Ratio?

Financial experts often recommend keeping your total EMIs under 40% of your monthly take-home salary. That ensures you have enough left for essentials, emergencies, and savings, without feeling stretched.

Example:

If your monthly income is ₹50,000, all your EMIs combined should ideally stay within ₹20,000. Anything beyond that could strain your finances or affect future loan eligibility.

Pro Tip

If you’re expecting a salary hike or bonus, consider a shorter tenure to save on interest.

If you’re managing multiple EMIs or an unstable income, pick a slightly longer term for peace of mind, you can always prepay later when things improve.

5. Verify the Lender’s Credibility Before You Apply

Every loan ad looks attractive: low interest, instant approval, minimal documents.

But before you share your personal details or upload KYC documents, always check if the lender is genuine and registered with the RBI.

Step 1: Confirm RBI Registration

Every legitimate lender in India must be either a bank or a registered NBFC (Non-Banking Financial Company). You can verify this directly on the RBI’s official NBFC list. It’s public and updated regularly.

If the name isn’t listed there, avoid sharing PAN, Aadhaar, or bank details, no matter how attractive the offer sounds.

Step 2: Watch Out for Red Flags

Many fraudulent or unregulated apps disguise themselves as instant loan providers. Here are a few tell-tale warning signs:

- Apps that demand excessive permissions, like access to contacts, photos, or location.

- No official website or registered address, a genuine lender always has both.

- “Advance fee” or “processing charge before approval”. This is the biggest red flag.

- Unverified domain emails. Avoid anything that doesn’t end with a proper company domain.

| Pro Tip RBI issued multiple advisories in 2023–24 urging users to borrow only from regulated entities after identifying over 400 fake digital lending apps on the Play Store. Source: RBI Press Release, August 2023 |

Banks vs NBFCs — Who Should You Choose?

| Banks | NBFCs | |

| Interest Rates | Lower, but stricter eligibility | Slightly higher, but faster approval |

| Approval Time | 2–5 working days | Often within 24 hours |

| Ideal For | Salaried professionals with strong credit | Self-employed or new-to-credit borrowers |

Tip: Compare both. NBFCs are often more flexible, especially if your CIBIL score is under 750 or you’re applying for a smaller ticket loan.

6. Evaluate Repayment Flexibility and Overall Experience

Getting a loan is easy today, but repaying it comfortably is what truly matters.

A good loan isn’t just about the approval speed or interest rate; it’s about how simple and stress-free your repayment journey feels.

What Makes a Loan Easy to Repay

Before you finalise your lender, check for these features that make a real difference:

- Auto-debit or UPI EMI options help you avoid missed payments and late fees.

- App-based EMI tracking lets you view your repayment schedule, outstanding balance, and due dates anytime.

- Foreclosure flexibility. Some lenders waive penalties after 12 EMIs; this helps you close your loan early and save on interest.

- Responsive customer support. A simple WhatsApp or call option can save you days of frustration when you need help.

Pro Tip

Before applying, check the lender’s Google Play Store or App Store ratings. Reviews often reveal if their EMI and support systems actually work as smoothly as they claim.

According to Experian India’s Consumer Credit Insights Report (2024), over 70% of Indian borrowers prefer lenders who offer flexible repayment or prepayment options, even if their interest rates are slightly higher.

It’s proof that for most people, peace of mind matters more than a 0.5% rate difference.

7. Compare on One Platform to See the Full Picture

When you check loan offers on different apps or websites one by one, you only see bits and pieces of the whole story. Some apps highlight low interest rates, others push fast disbursal, and some don’t show fees until the very end.

And if each lender is pulling your credit report separately, it can even lead to multiple hard inquiries, which may temporarily bring down your CIBIL score.

A comparison platform solves this problem by showing everything in one place clearly and honestly, without affecting your score multiple times.

Why Comparing in One Place Helps

Instead of juggling 8–10 tabs, a trusted platform like Match My Money lets you:

- View offers from multiple RBI-registered lenders side by side

- See key details upfront, like interest rate, processing fee, maximum loan amount, tenure, disbursal time

- Understand which lender matches your salary, credit profile, and requirement

- Avoid duplicate calls, random approvals, and misleading “instant” ads

- Protect your credit score by checking all offers through a single soft inquiry

It’s faster, safer, and helps you make an informed choice without unnecessary stress.

Example: Why a “Higher Rate” Isn’t Always Costlier

Priya, a 29-year-old marketing executive from Pune earning ₹60,000/month, needed a ₹2 lakh loan for a medical emergency.

Here’s what she found when she compared the full details:

| Criteria | Lender A | Lender B |

| Interest Rate | 10.75% | 11.25% |

| Processing Fee | 3% | 1% |

| Tenure | 3 Years | 2 Years |

| Total Cost (Approx.) | ₹2,23,600 | ₹2,21,300 |

Even though Lender A showed a lower interest rate, Lender B actually cost less overall because of a smaller fee and shorter tenure.

This is exactly why comparing everything together, not just the rate matters so much.

Choose a Loan That Works for You

There’s no such thing as a “perfect” personal loan for everyone.

What really matters is whether the loan you choose fits your income, your comfort, and your plans for the next few years.

When you compare thoughtfully, looking at the full cost, the fees, the tenure, and the lender’s credibility, the decision becomes much clearer. And once you see the complete picture side by side, it’s easier to pick the option that won’t create stress later.

A good loan should do one simple thing: help you move forward without worrying about hidden surprises.