Short Answer

No, you do not always need a CIBIL score to get a personal loan in India.

First-time borrowers without a credit history may still get a loan, but approval depends on factors like income stability, bank behaviour, and the lender’s risk policy.

A Common Question First-Time Borrowers Ask

A common question many first-time borrowers ask is:

“Can I get a personal loan without a CIBIL score?”

The short answer is: Yes, it’s possible, but not always easy.

To understand why, let’s start with the basics.

What Is a CIBIL Score?

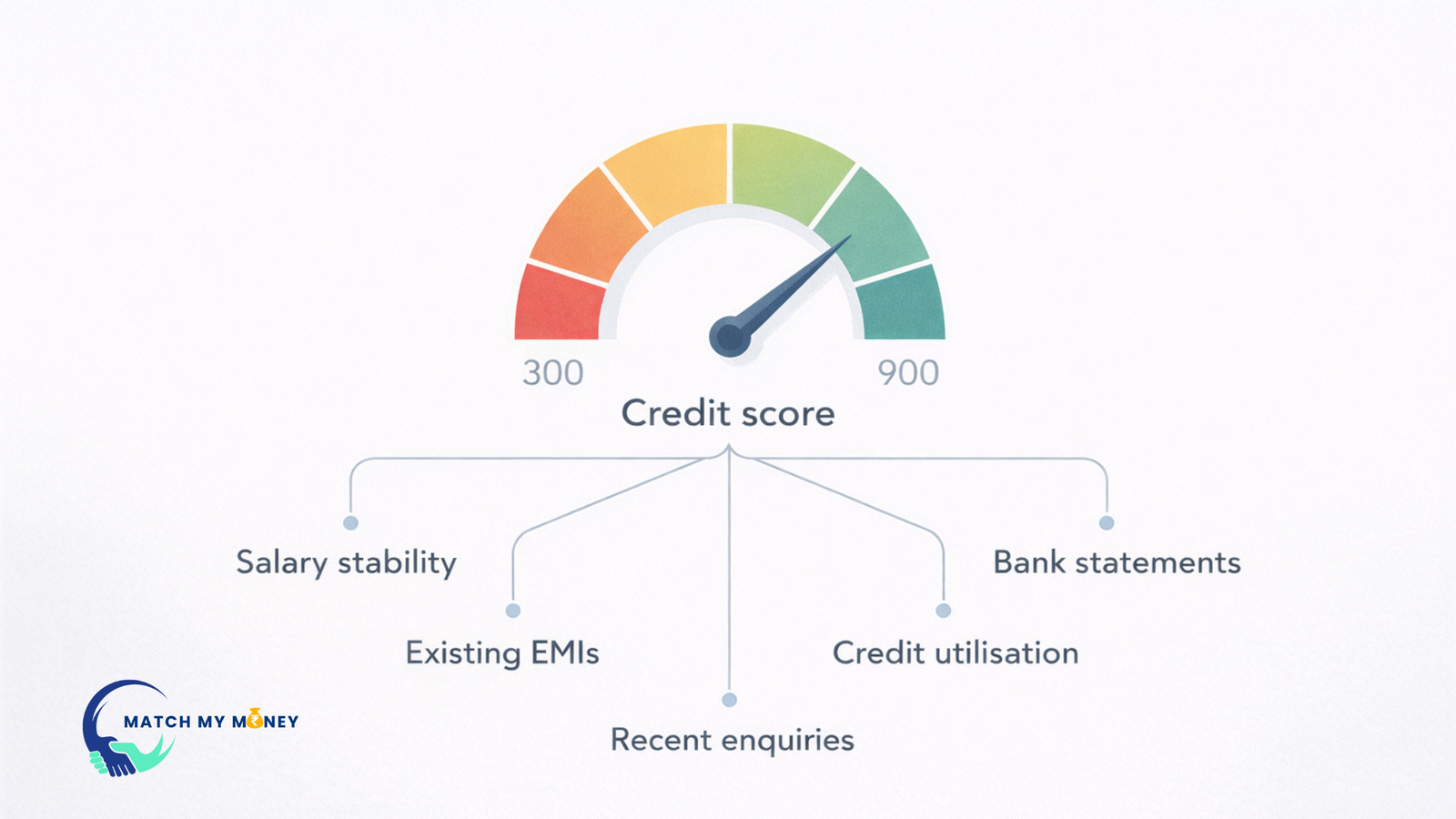

A CIBIL score is a three-digit number between 300 and 900 that reflects how you’ve handled credit in the past.

It is generated by TransUnion CIBIL, one of India’s major credit bureaus, using your loan and credit-card repayment data.

In simple terms, it answers one question for lenders:

How reliably does this person repay borrowed money?

Why Is CIBIL Important for Personal Loans?

Most lenders (banks, NBFCs, fintechs) prefer applicants with a CIBIL score of 700+ because it signals lower risk.

A strong score helps you get:

- Faster approval

- Higher loan amounts

- Lower interest rates

- Fewer document checks

But here’s something many people don’t know:

Having no CIBIL score is not the same as having a bad CIBIL score.

Someone who has never taken a loan may not have a score at all, this is called a thin file.

No CIBIL Score vs Low CIBIL Score (Big Difference)

If you’ve never taken a loan or credit card, you may have no credit history at all.

This is often called a thin file.

From a lender’s perspective:

- No score = unknown risk

- Low score = known repayment issues

This is why first-time borrowers are sometimes approved, while people with poor repayment history get rejected — even if both earn similar salaries.

How Your CIBIL Score Affects Loan Approval

Your CIBIL score isn’t the only factor lenders look at. They also check:

- Salary and employer stability

- Bank statements

- Existing EMIs

- Credit utilisation

- Recent loan inquiries

But your CIBIL score sets the tone:

A higher score = smoother journey.

A lower or missing score = more cautious evaluation.

This is why some applicants with decent salaries still face rejections because lenders see risk in the credit pattern, not the income.

If you want to understand how to check your loan eligibility safely without accidentally lowering your score, this guide explains it clearly:

Read: How to Check Personal Loan Eligibility Without Hurting Your CIBIL Score

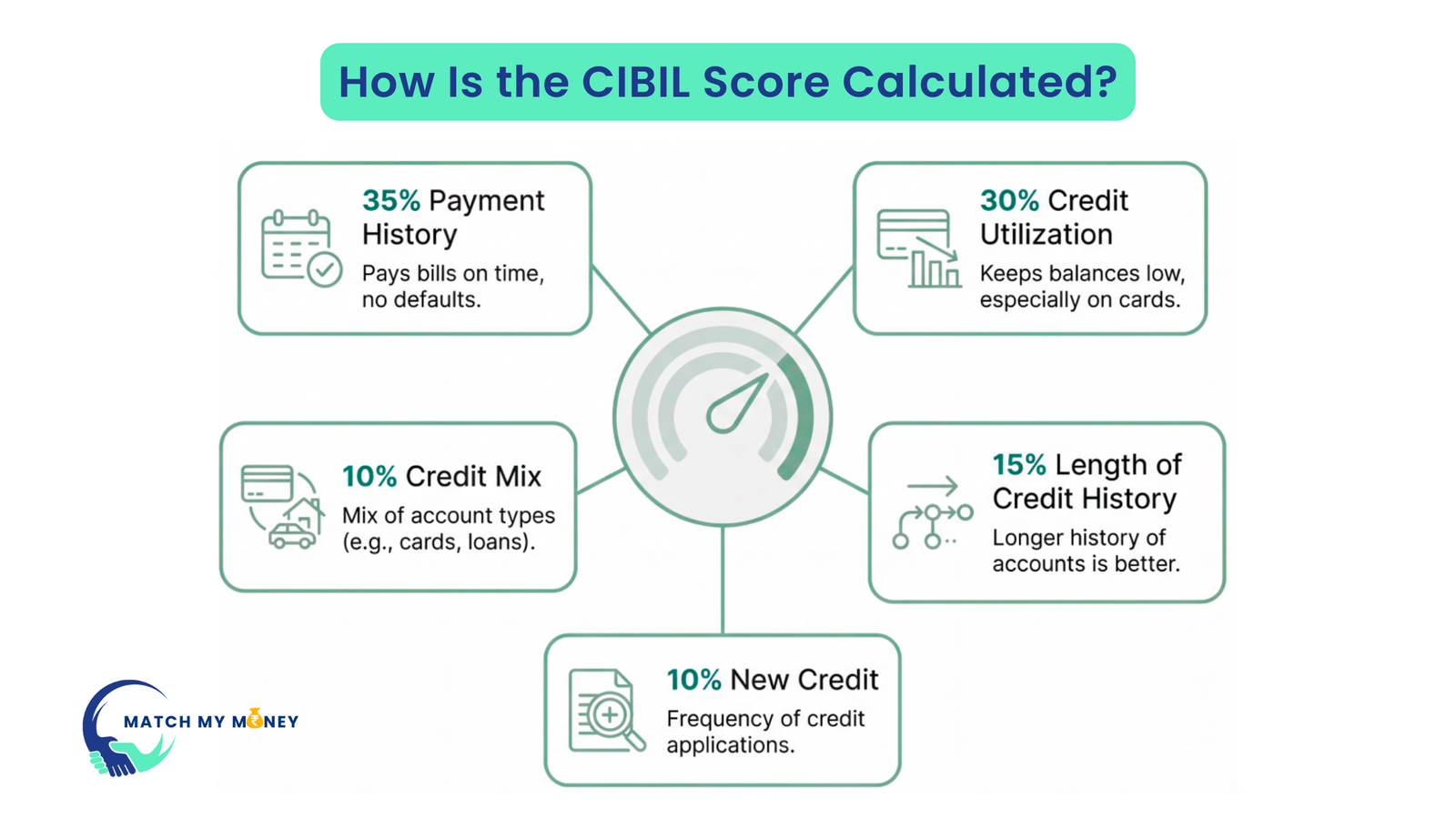

How Is the CIBIL Score Calculated?

CIBIL uses multiple factors to calculate your score:

1. Payment History (35%)

On-time vs late EMI/credit card payments.

2. Credit Utilisation (30%)

How much of your credit limit you use regularly.

3. Length of Credit History (15%)

How long you’ve been using loans/credit cards.

4. Credit Mix & Types (10%)

A balance of secured and unsecured loans.

5. Recent Inquiries (10%)

Multiple loan applications in a short period can pull your score down.

Once you understand how your score is calculated, the next step is learning how to compare different loan offers correctly so you choose the one that truly fits your profile.

Read: How to Compare Personal Loan Offers Like a Pro

How to Check Your CIBIL Score in India

You can check your score:

- For free on the official CIBIL website

- Through bank apps

- Through credit-monitoring apps

- On financial platforms

It takes just a few minutes and helps you understand where you stand before applying.

Can I Get a Personal Loan Without a CIBIL Score?

Yes, especially from digital lenders and NBFCs.

But terms may not be as favourable as someone with a strong score.

Here’s what can help if you don’t have a score:

- A stable salary

- Clean bank statements

- Low financial obligations

- Strong employer category

- Good repayment history on BNPL or card EMIs

Today, many lenders offer loans to first-time borrowers using alternate data like salary patterns and spending behaviour.

But comparing lenders becomes crucial because each one treats “no score” differently.

Bottomline – Do You Need a CIBIL Score?

Not always. But it definitely helps.

If you have a good score → you get better rates.

If you don’t → you may still get a loan, but you need to pick lenders wisely.

And this is where safe comparison becomes extremely important.

A Simple Way to Move Forward

Whether you have a strong CIBIL score or no score at all, the smartest first step is understanding which lenders are most likely to approve you, without hurting your credit.

Match My Money helps you get a clearer picture of your borrowing options by comparing loan offers from multiple trusted lenders side by side. No repeated hard inquiries, no guesswork, just accurate insights.

Want to know which lenders suit your profile?

Compare personal loan options without repeated credit checks.