When most people look at a personal loan, they look at one thing first.

The EMI.

That’s not because they’re careless. It’s because EMI feels like the safest way to judge a loan.

Lower EMI means:

- Less pressure every month

- Easier budgeting

- More breathing room

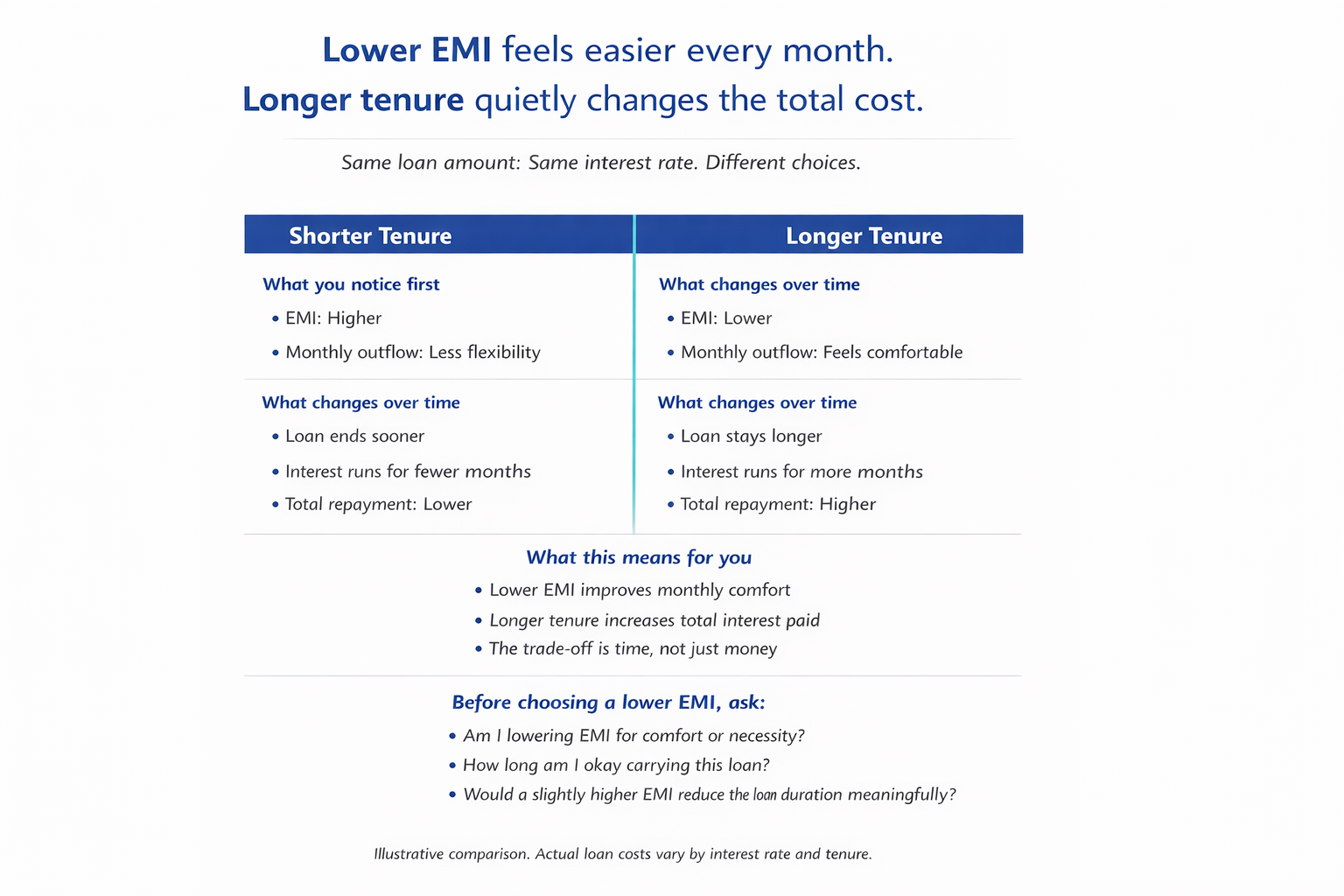

On the surface, it feels like the responsible choice. But here’s the part many borrowers only realise much later: A loan that feels comfortable month-to-month can quietly cost more overall.

Why EMI Feels Like the Right Decision

Monthly expenses are real. Rent, groceries, school fees, subscriptions, everything competes for the same salary.

So when a lender says, “We can lower your EMI by extending the tenure,” it sounds helpful. It tells you no stress, no tight months, no lifestyle disruption. Choosing the lower EMI makes complete sense.

The problem isn’t the thinking. It’s what the thinking misses.

What Changes When Tenure Increases

Your EMI doesn’t exist on its own. It’s connected to three things:

- Loan amount

- Interest rate

- Loan tenure

When EMI is reduced without changing the loan amount or interest rate, one thing almost always increases:

Time.

More months mean:

- Interest is charged for longer

- Repayment stretches further into the future

Nothing dramatic happens in a single month. The difference shows up slowly, over time. That’s why this trade-off is easy to miss.

The Quiet Effect of “Just a Few Extra Months”

A longer tenure doesn’t feel risky. There’s no warning sign. No sudden jump in EMI. No moment where the loan feels “wrong”.

Instead:

- The loan simply stays with you longer

- Interest keeps adding up quietly

Month by month, everything feels fine. Until you look back and realise: “I paid much more than I expected for this.” Not because the loan was bad. But because the timeline stretched.

Why This Catches Even Careful Borrowers Off Guard

Most borrowers are not reckless.

They:

- Check eligibility

- Look at interest rates

- Make sure EMI fits their income

But very few people ask: “How much will this loan cost me in total if I choose this EMI?”

That question feels abstract compared to a concrete monthly number. So people optimise for what they can feel – monthly comfort and ignore what they can’t immediately see the total cost.

A Simple Way to Think About It

Think of EMI like pace.

A slower pace feels easier while walking. But if you slow down too much, the journey simply takes longer. Longer journeys cost more energy. Loans work the same way.

Lower EMI = slower pace

Longer tenure = longer journey

Longer journey = higher total cost

Once you see it this way, the trade-off becomes clearer. This isn’t a mistake. It’s human behaviour.

When a Lower EMI Does Make Sense

Lower EMI is not always a bad choice. In fact, there are situations where it’s the smarter option.

For example:

- If your income is irregular

- If you expect major expenses in the near future

- If you’re protecting cash flow during a transition period

In these cases, stability matters more than speed. A slightly higher total cost can be worth it if it prevents:

- Missed EMIs

- Financial stress

- Dependence on other credit

The key difference is intentional choice. Lower EMI works best when chosen deliberately, not automatically.

The problem is default thinking

Where people get into trouble is not by choosing a lower EMI. It’s by choosing it by default.

No comparison, no consideration of tenure, no look at the full repayment picture.

Just: “This EMI fits. Let’s go with it.”

That’s when loans quietly become more expensive than expected.

A Better Way to Decide

Instead of asking only: “Can I afford this EMI?”

Also ask:

- How long will I be repaying this loan?

- How much extra am I paying for lower monthly comfort?

- Would a slightly higher EMI reduce the total cost meaningfully?

You don’t need complex calculations. You just need to see the options side by side. This is why comparing personal loan offers properly makes such a difference.

Why This Matters Before You Apply

Once a loan is taken, choices narrow. Changing tenure later isn’t always easy. Closing a loan early may involve charges. Refinancing depends on eligibility.

That’s why this thinking matters before applying. A few extra minutes of comparison can save months or years of unnecessary interest.

If You Want the Full Picture

This article focuses on one idea: why lower EMI can quietly increase total cost.

If you want a clear, complete understanding of how EMI, interest rate, and loan tenure work together, this guide explains it calmly and simply: Taking a Personal Loan? Read This Once Before You Decide

Understanding the full picture doesn’t make loans complicated. It makes decisions clearer.

Final Thought

Lower EMI feels safe because it protects the present. Shorter tenure feels harder because it asks more from you now.

The smartest loan choice isn’t about choosing one over the other. It’s about knowing what you’re trading, and deciding consciously. That awareness alone puts you ahead of most borrowers.