Already paying one personal loan EMI and wondering if you can take another?

Many borrowers assume approval depends only on income or credit score. In reality, lenders judge a second personal loan very differently. Once you already have an active loan, lenders start looking at patterns – how stable your repayments are, how stretched your monthly budget feels, and whether your financial position has improved or worsened since your first loan.

A second personal loan can be a sensible decision in some situations. In others, it quietly increases rejection risk, total interest cost, and long-term stress, even if the EMI looks manageable on paper.

This guide explains how lenders actually think, when taking a second personal loan can work, when it’s better to wait, and what to fix before you apply, so you can decide without damaging your credit or finances.

Is It Legal and Possible to Have Multiple Personal Loans in India?

Yes.

There is no law in India that stops you from having multiple personal loans at the same time.

But legality is not the issue. Approval is.

Banks and NBFCs will approve a second loan only if your profile still looks safe after adding one more EMI.

A few important facts:

- Lenders decide approval based on risk checks, not “number of loans”.

- Your existing personal loans are visible in your credit report.

- New loans and repayments are reported to credit bureaus regularly, so lenders can see recent borrowing activity.

- Applying from a different bank does not “hide” your current loan.

So while it is legal to take a second or even third personal loan, approval depends entirely on how your overall profile looks to lenders.

The Real Question Isn’t “Can You”, It’s “Will Lenders Approve?”

Legality answers “is it allowed?”

Lenders care about “can this person safely repay more?”

Once you already have a personal loan, lenders stop looking at you as a fresh borrower. They start checking whether your financial situation has improved, stayed stable, or worsened since your first loan.

This is why two people with the same income can get very different outcomes when applying for a second loan.

If you remember only one thing, remember this: a second loan is approved when your finances look stable after adding the new EMI, not before.

How Lenders Evaluate a Second Personal Loan

When you apply for a second personal loan, lenders evaluate you more strictly than they did the first time. Not because a second loan is automatically risky, but because risk compounds once one EMI already exists.

Instead of looking at one number or rule, lenders look at patterns: how your income, EMIs, repayment behaviour, and borrowing history work together.

Here’s how that evaluation actually works.

1. Credit Behaviour, Not Just the Score

A good credit score helps, but lenders focus more on recent behaviour.

They check:

- Have you paid every EMI on time?

- Any delays in the last 6–12 months?

- Any settlements or restructuring?

A borrower with a 730 score and perfect repayment history often looks safer than someone with a 780 score and recent delays.

What this means for you:

If you’ve had any late EMI recently, waiting and rebuilding a clean repayment streak improves approval chances more than applying again quickly.

2. Your EMI Load Compared to Income

Lenders calculate how much of your monthly income is already committed to EMIs, across all obligations.

This includes:

- Personal loans

- Home or car loan

- Credit card EMIs

- Buy-now-pay-later commitments

As a general practice:

- Upto ~30–35% → comfortable

- Around 40% → cautious

- Above that → high risk

But lenders don’t stop at ratios.

What this means for you:

If your EMIs leave you stretched by the middle of the month, your profile already looks tight, even if the ratio seems acceptable on paper.

3. Existing Loan Obligations Change How You’re Viewed

Once you already have an active personal loan, lenders stop treating you like a fresh borrower.

They assess:

-

How many loans are currently active

-

How much principal is still outstanding

-

Whether you’ve meaningfully reduced debt since the first loan

Borrowers who have repaid a substantial portion of their first loan are seen as more stable than those whose loan has just begun.

What this means for you:

If your first loan is still new, a top-up with your existing lender (bank or NBFC) often has higher approval odds than a completely new second loan.

4. Income Stability and Growth Carry Strong Weight

Lenders look at whether your income can reliably support multiple EMIs.

For salaried borrowers, this includes:

-

Job stability

-

Time with current employer

-

Predictability of income

For self-employed borrowers, consistency of earnings matters more than short-term spikes.

What this means for you:

Income growth after your first loan works strongly in your favour.

Taking on more debt without income stability works against you.

5. Recent Credit Activity Signals Risk or Control

Lenders closely track:

-

How many loan or card applications you’ve made recently

-

How close together those applications were

Multiple applications in a short span signal urgency or financial stress, not confidence.

What this means for you:

Applying to several lenders “just to check” can quietly reduce approval chances. Shortlisting one or two suitable options and applying once is safer.

6. Lender Policies and Existing Relationships Matter

Beyond your personal profile, each lender has internal rules.

Some may:

-

Prefer top-ups over new loans

-

Require partial repayment before approving another loan

-

Be more flexible with existing customers

Others may apply stricter thresholds if you already have loans elsewhere.

What this means for you:

Approval isn’t just about eligibility, it’s about matching your profile to the right lender, not applying everywhere.

7. Purpose of the Second Loan Still Shapes Risk

While personal loans are flexible, lenders still assess whether additional borrowing looks sensible.

A second loan used for:

-

Medical expenses

-

Essential repairs

-

Debt consolidation

is viewed differently from borrowing that simply increases lifestyle spending without improving income.

What this means for you:

Borrow only what you genuinely need. Loans taken without a clear purpose increase both rejection risk and long-term stress.

In simple terms

A second personal loan is approved when your finances still look stable after adding the new EMI, not just before.

Should You Take a Second Personal Loan? A Quick Decision Check

Green Zone: You Can Consider Applying

- Total EMIs are within ~30–35% of take-home income

- No EMI delays in the last 6 months

- Income has increased after your first loan

- You’ve already repaid a meaningful part of the first loan

- The second loan is for a real need (not lifestyle or short-term cash gap)

Yellow Zone: Pause and Fix 1–2 Things First

- EMIs are closer to ~40% of take-home pay

- You’ve applied for credit recently

- Your first loan is still new

- You’re not sure how you’ll handle a bad month (medical, job change, emergency)

Red Zone: Don’t Apply Right Now

- You’re taking the second loan mainly to manage existing EMIs

- You’ve had a missed/late EMI recently

- Your budget has no buffer after EMIs

- Income hasn’t grown but debt has

This won’t just improve approval chances, it prevents a second loan from becoming a long-term stress.

Situations Where a Second Personal Loan Can Work

A second loan is not always a bad decision. It can make sense when:

- Income has clearly increased after the first loan

- The first loan is nearing completion

- The new loan replaces higher-cost debt

- The purpose is time-sensitive and unavoidable (medical, essential repairs)

In these cases, lenders often see the second loan as manageable, not reckless.

Example: If you took your first loan two years ago, your income has increased, and you have a clean repayment record, a second loan for a medical expense may be treated as manageable.

Pros and Cons of Taking Multiple Personal Loans (Quick View)

When it works

-

Helps meet unavoidable or time-sensitive needs

-

Can replace higher-cost debt if structured carefully

-

May strengthen credit if all EMIs are paid on time

Where it backfires

-

Monthly cash flow becomes tight with little buffer

-

Total interest cost rises quietly over time

-

One missed EMI can undo years of good credit

-

Future loan eligibility (home, car) may reduce

Multiple loans are not the issue. Poor structure is.

If You Already Have Multiple Personal Loans, Manage Them Smarter

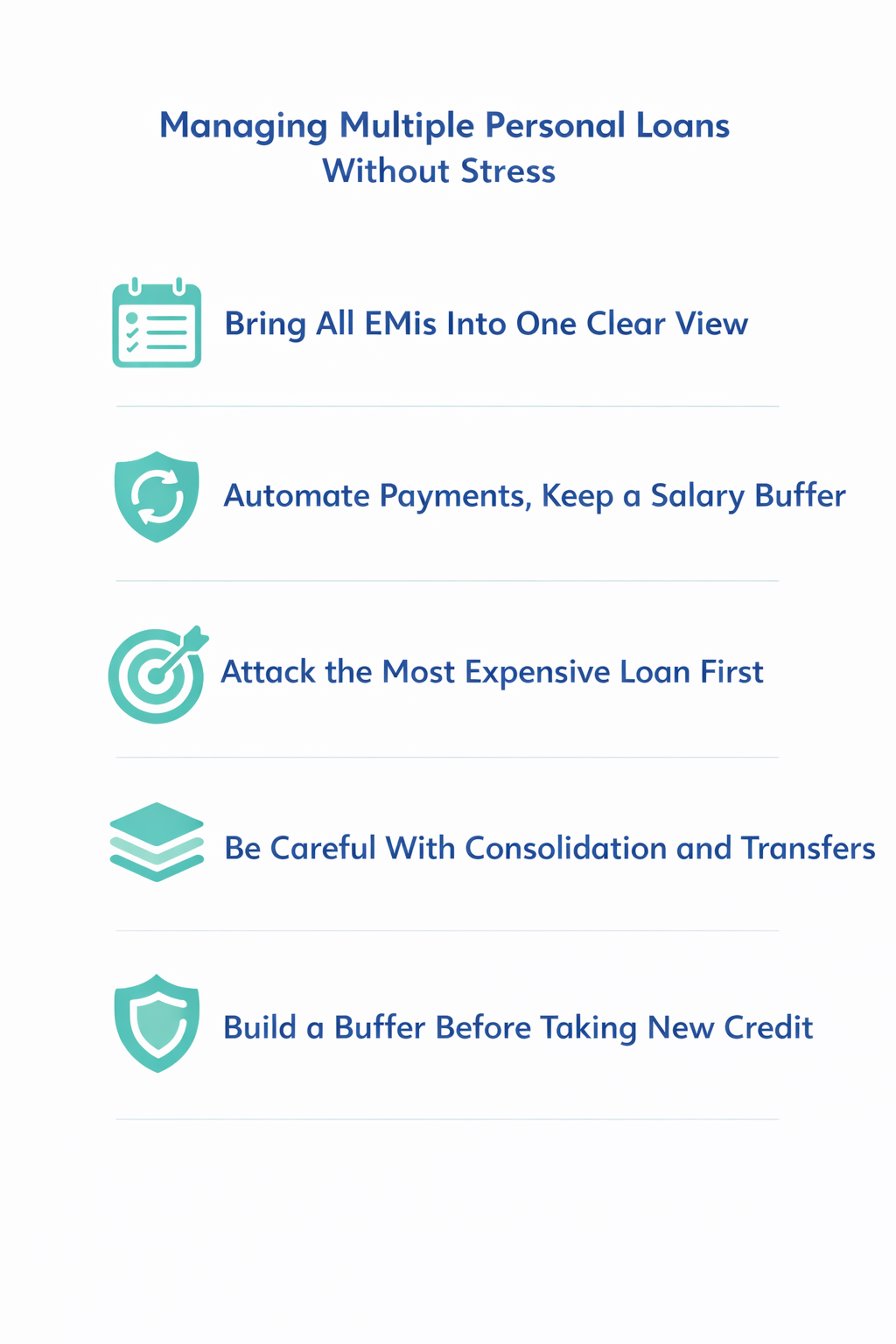

Having more than one personal loan is not the problem. Losing control over timing, cash flow, and buffers is. If you’re already juggling multiple EMIs, focus on these fundamentals first.

1. Bring All EMIs Into One Clear View

When loans are scattered across apps and dates, missed EMIs become accidental, not intentional.

What to do:

-

List every EMI amount and due date in one place

-

Use a single calendar or reminder system

-

Treat one missed EMI as a serious event, not a small delay

This alone prevents the biggest credit score damage.

2. Automate Your Payments But Keep a Salary Buffer

Automation works only if your account always has room.

What to do:

-

Enable auto-debit for all EMIs

-

Keep a buffer equal to one full EMI cycle after salary credit

-

Avoid setting EMIs so tight that one unexpected bill causes a bounce

Automation should reduce stress, not create it.

3. Attack the Most Expensive Loan First

Multiple loans quietly increase interest cost over time.

What to do:

-

Continue all EMIs as scheduled

-

Use bonuses, savings, or surplus to prepay the highest-interest loan

-

Even small extra payments shorten tenure and reduce total cost

This is where long-term savings actually come from.

4. Be Careful With Consolidation and Balance Transfers

Consolidation can help but only if it genuinely simplifies things.

What to do:

-

Consolidate only if it lowers total interest or reduces EMI stress

-

Account for processing fees and foreclosure charges

-

Avoid “consolidation” that simply resets tenure and hides cost

Lower EMI alone is not success. Lower total burden is.

5. Build an Emergency Buffer Before Taking Any New Credit

Multiple EMIs leave little margin for bad months.

What to do:

-

Aim for at least 3 months of expenses + EMIs as emergency savings

-

Pause new borrowing until this buffer exists

-

Without a buffer, even a small disruption can cause a chain reaction

Emergency funds prevent loans from turning into traps.

Common Mistakes That Make a Second Loan Backfire

Most second personal loans don’t fail because of one big mistake.

They fail because of small decisions that add up quietly.

Here are the mistakes lenders see most often.

1. Applying Everywhere to “See What Happens”

Many borrowers apply to multiple lenders hoping one will approve.

What actually happens:

-

Multiple credit enquiries pile up

-

Your profile starts looking urgent or stressed

-

Approval odds drop instead of improving

Better approach:

Shortlist one or two suitable options and apply once, with confidence.

2. Taking a Second Loan Without Income Growth

A second loan works best when income has improved after the first one.

When debt grows but income doesn’t:

-

EMI pressure increases month by month

-

Approval risk rises for future loans

-

One bad month can derail everything

Rule of thumb:

If income hasn’t grown, reduce debt first — then apply.

3. Choosing a Longer Tenure Just to Lower EMI

Lower EMI feels safe.

Longer tenure quietly increases total cost and keeps you in debt longer.

This often leads to:

-

Paying much more interest than expected

-

Staying loan-heavy even when income improves

Better mindset:

Choose tenure you can manage and exit early if possible.

4. Using New Loans to Manage Old EMIs

Taking a new loan to pay an existing EMI is a warning sign.

This is how debt spirals begin:

-

Old problems are postponed, not solved

-

Total debt increases due to fees and interest

-

Stress builds instead of reducing

If EMIs feel unmanageable, restructuring or consolidation (done carefully) is safer than rolling debt forward.

5. Ignoring the “Bad Month” Test

Many loans look affordable in a perfect month.

The real question is: What happens if one unexpected expense hits?

If one medical bill, delay in salary, or emergency forces you to juggle EMIs, the structure is already fragile.

Strong loans survive bad months, not just good ones.

Avoid Approval Mistakes by Checking Eligibility First

Applying blindly is one of the easiest ways to hurt approval chances. Every rejected application leaves a signal.

A safer approach is to:

-

Shortlist lenders that fit your profile

-

Compare EMI and total cost

-

Apply once, with confidence

Match My Money helps you compare eligible personal loan options in one place, so you can choose what fits your repayment comfort — not just what looks cheapest on paper.

Final Thought

A second personal loan isn’t good or bad by default.

It works when income, timing, and EMI comfort support it. It backfires when used to stretch a tight month.

The smartest borrowers don’t ask, “Can I get another loan?”

They ask, “Will this still feel okay in a bad month?”