Updated for FY 2025-26 (Assessment Year 2026-27)

January and February are when most salaried employees in India are asked to choose between the old vs new tax regime and declare investments.

Most people treat this as a formality. They shouldn’t.

Because this one decision directly affects:

- how much tax your employer deducts every month

- your take-home salary for the rest of the year

- whether you end the year with a refund or a surprise tax bill

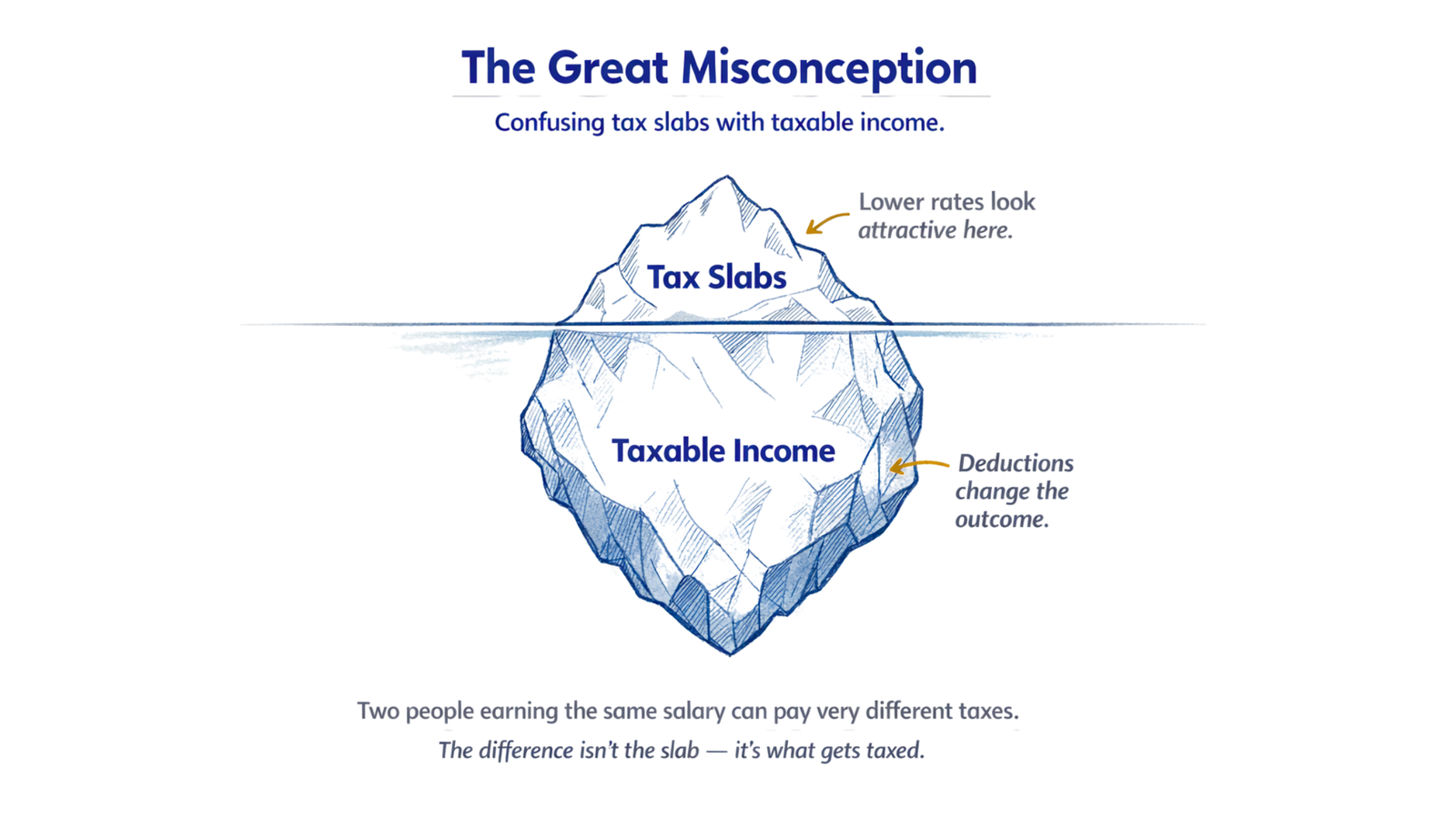

The confusing part isn’t the choice itself. It’s that there is no single “right” tax regime.

The correct option depends on:

- how your salary is structured

- whether you pay rent

- PF deductions

- insurance, home loans, and other real commitments

Not just tax slabs.

This guide explains how salaried employees should choose between the old vs new tax regime for FY 2025–26, so you can make the decision before the declaration deadline, without regret.

Why This Decision Matters More Than It Feels

When HR asks you to choose a tax regime and declare investments, it can feel like an internal formality.

It isn’t.

What Actually Happens After You Submit Your ChoiceOnce you select a tax regime:

|

If you choose a regime that results in higher tax:

- your monthly in-hand salary drops immediately

- that money is already gone from your paycheck

Most employers do not recalculate TDS mid-year unless there’s a major correction.

“Can’t I Fix This While Filing My ITR?”Yes, but with limitations. When you file your income tax return:

But:

|

Choosing the wrong regime now means lending your money to the government interest-free for months.

That’s not smart cash-flow management.

Why “I’ll Decide Later” Usually BackfiresChoosing between tax regimes is not about slabs. It’s about: How much of your salary is actually taxable after accounting for your existing financial reality. Two people earning the same salary can pay very different tax, purely because:

With that lens, let’s look at both regimes properly. |

The Old Tax Regime: Who It Rewards (And Why)

The Old Tax Regime isn’t complicated. It’s behaviour-based.

It assumes one simple thing:

| If you’re already spending or committing money towards long-term stability, healthcare, housing, and family responsibilities, you should be taxed less. |

What the Old Regime Recognises

- HRA (House Rent Allowance)

- PF and other 80C deductions (up to ₹1.5 lakh)

- Health insurance (80D)

- Home loan interest

- Certain family-related deductions

If these already exist in your life, the old regime often works in your favour.

HRA: The Biggest Divider

If you pay rent and receive HRA, this alone can change the outcome.

Under the old regime: a significant portion of rent reduces taxable income

Under the new regime: HRA is ignored entirely

If you live in a metro and rent is a meaningful expense, ignoring HRA almost guarantees a wrong comparison.

PF and 80C: Deductions You Already Have

Many salaried employees think: “I didn’t invest much, so old regime won’t help.”

That’s usually incorrect.

Employee PF contributions automatically count under Section 80C. You don’t need to “do something extra” to claim them, they already exist. Ignoring PF while comparing regimes leads to distorted results.

Health Insurance (80D)

If you pay:

- your own health insurance

- or your parents’ health insurance

These are real cash outflows that:

- reduce taxable income under the old regime

- do not exist at all under the new regime

Home Loan Interest

For self-occupied houses:

- the old regime allows deduction of interest paid

- the new regime removes this benefit entirely

For homeowners, especially in early loan years, this can swing the decision decisively.

Who the Old Regime Usually Works Best ForThe old regime tends to make sense if two or more of these apply to you:

|

Notice the pattern:

It rewards existing commitments, not aggressive tax planning.

The Most Common Mistake with the Old Regime

The biggest mistake is assuming: “Old regime only works if I aggressively invest for tax saving.”

That’s not true. The old regime works best when:

- your life stage already involves commitments

- your salary structure includes benefits

- and you acknowledge those before choosing

If you ignore what you already qualify for, the old regime will always look worse than it actually is.

This is also why comparing tax regimes only by slab rates often leads to the wrong conclusion.

Tax slabs apply after your taxable income is calculated. Deductions like PF, HRA, insurance, and home loan interest change how much of your salary is actually taxed. Two people earning the same salary can fall in the same slab and still pay very different tax — purely because their taxable income is different.

The New Tax Regime: Why It Looks Attractive (And When It Works)

The New Tax Regime was introduced to solve a real problem. For years, salaried employees complained that:

- tax planning was confusing

- deductions felt forced

- and saving tax meant buying products they didn’t fully understand

The new regime flips that logic. Instead of asking “What deductions do you have?”, it asks: “Do you want lower tax rates and fewer conditions?”

That’s why it feels cleaner and why many people instinctively gravitate toward it. But clean structure does not always mean lower tax.

What the New Regime Actually Rewards

The new regime rewards financial simplicity.

It works best when your income is not already tied up in rent, loans, or structured deductions, when most of your salary flows directly to you without needing exemptions to make the math work.

The new regime tends to suit people who:

- do not pay rent or do not receive HRA

- do not have a home loan

- do not actively use deductions like 80C or 80D

- are comfortable paying tax on a larger portion of income in exchange for lower slab rates

- prioritise flexibility and monthly liquidity over structured saving

Lower Slabs ≠ Lower Tax (Always)

Most comparisons stop at slab rates and that’s where confusion begins.

Yes, the new regime has more slabs, lower incremental rates, and a higher standard deduction. But tax is calculated on taxable income, not on salary.

Under the old regime, deductions reduce your taxable income before slabs apply. Under the new regime, you give up those reductions entirely.

So the real question isn’t: “Which slab is lower?” It’s: “How much of my income is actually being taxed?”

If a meaningful part of your salary would have been reduced by HRA, PF, insurance, or loan interest, slab rates alone can be misleading.

Why the New Regime Feels Better During the Year

One reason people like the new regime is psychological.

Because:

- fewer deductions are considered

- projected tax is simpler

- TDS often feels more predictable

- Declarations are minimal

This can result in:

- slightly higher monthly in-hand salary

- less paperwork during the year

- fewer surprises caused by mismatches between declared and actual deductions

But it is important to separate monthly visibility from annual cost. Higher in-hand salary during the year does not automatically mean lower tax overall. It only means the tax calculation is simpler.

The Hidden Trade-off Most People Miss

When you choose the new regime, you are effectively saying: “I’m okay giving up deductions in exchange for lower slab rates.”

That’s a valid choice if you’re truly not using those deductions. The mistake happens when:

- PF is already deducted but ignored in comparison

- insurance premiums are already paid but not counted

- rent is paid but HRA isn’t factored in

In these situations, the new regime appears better not because it is cheaper, but because the comparison is incomplete. You are not saving tax, you are overlooking what you already qualify for.

Who the New Regime Usually Works Best ForThe new regime generally makes sense if most of the following apply:

For these profiles, the new regime can genuinely result in lower tax with less effort. |

A Final Caution

The most common mistake is choosing the new regime simply because “I didn’t invest this year anyway.”

Tax decisions are not about intentions. They are about what already exists.

The new regime works best when your financial life is genuinely simple — not when it is rushed, unclear, or under-examined.

Old vs New Tax Regime: Practical Comparison

| Your Situation | What This Means in Practice | Regime That Usually Fits Better |

| You pay rent and receive HRA | Rent is a fixed monthly cost; HRA can meaningfully reduce taxable income | Old Regime |

| PF is deducted every month | You already have 80C deductions, whether you planned them or not | Old Regime |

| You pay health insurance for self or parents | These are unavoidable expenses that qualify as deductions | Old Regime |

| You are repaying a home loan | Interest is a fixed commitment that gets recognised | Old Regime |

| You live in an owned house (no rent) | No HRA benefit to factor in | New Regime |

| You have minimal or no deductions | Lower slabs and simplicity matter more | New Regime |

| You prefer higher monthly take-home salary | Fewer adjustments through deductions | New Regime |

| You’re early in your career with few commitments | Financial life is relatively simple | New Regime |

Important:

“Usually fits better” does not mean “always fits better.”

This table is a directional guide, not a shortcut.

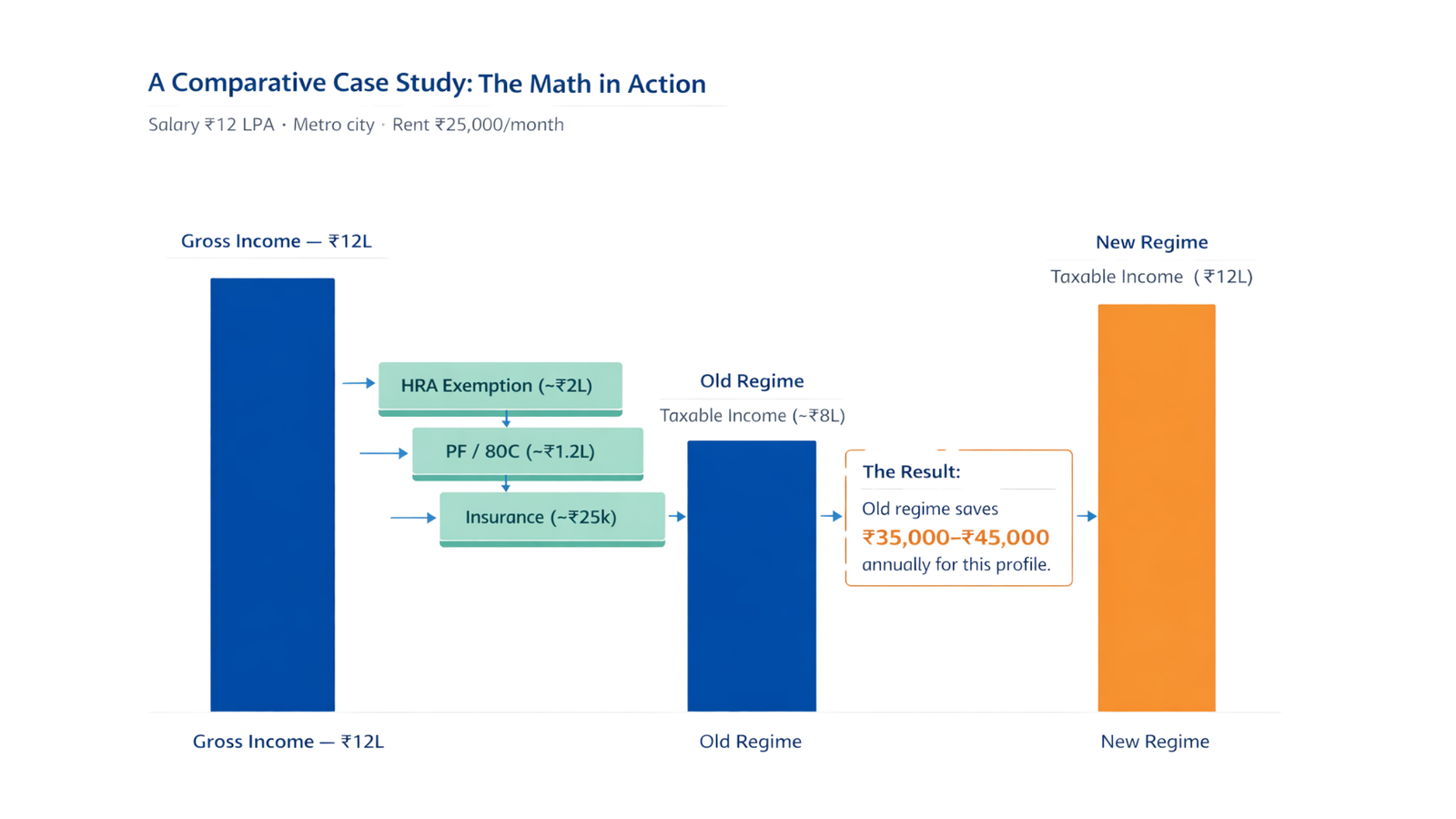

A Simple Example (That Shows the Difference)

Profile: ₹12 LPA salary, metro city, rent ₹25,000/month

Old Tax Regime

- HRA exemption: ~₹2 lakh

- PF (80C): ~₹1.2 lakh

- Health insurance (80D): ~₹25,000

Total deductions/exemptions: ~₹3.5–4 lakh

→ Taxable income drops before slabs apply

New Tax Regime

- HRA, 80C, and 80D don’t apply

- Tax is calculated on a much larger portion of income

Result:

For this profile, old regime tax is lower by ~₹35,000–₹45,000 annually.

This difference doesn’t show up when you compare slabs. It shows up when you compare taxable income.

A Small but Critical Reminder

This comparison works only if you count deductions you already have, not ones you plan to make later.

If you haven’t actually paid insurance premiums, invested money, or incurred eligible expenses, those deductions don’t exist yet and shouldn’t be included.

A Quick Scenario Check (Does This Sound Like You?)

If one of these situations feels familiar, it usually points you in a direction but always confirm with a calculation.

1. Early Career, Metro City, Paying Rent

If you pay rent and have PF deducted from salary, the old regime often works out better than expected once HRA and PF are counted, even if the new regime feels simpler month to month.

2. Insurance, Family Responsibilities, or a Home Loan

If your finances include insurance premiums, dependent family members, or EMIs, the old regime usually deserves serious consideration because it recognises these existing commitments.

3. High Income, Few Deductions

If you live in your own house, have no home loan, and don’t actively use deductions, the new regime’s lower slab rates can sometimes be comparable or even better. Income alone doesn’t decide the regime, deductions do.

4. Unsure and Short on Time

Defaulting to the new regime because of uncertainty often leads to higher TDS during the year and delayed refunds later. When in doubt, pause and calculate once instead of guessing.

How to Decide in 10 Minutes (A Practical Checklist)

You don’t need to “understand tax” to choose correctly. You just need to compare the two regimes using your actual deductions, not assumptions.

Keep your latest salary slip / Form 16 estimate and your investment declaration list open.

Step 1: Identify Deductions You Already Have (Not What You Plan to Do)

Write down what is already happening in your finances:

- PF is deducted from your salary (check payslip → “PF/EPF”)

- You pay rent and receive HRA (check salary structure → “HRA”)

- You have health insurance premiums you pay (self and/or parents)

- You pay home loan interest (only if you have a home loan)

- You already invest in 80C instruments (ELSS, LIC, PPF, tuition fees, etc.)

Step 2: Add Up Your Likely Deductions (Quick Estimate is Enough)

You don’t need perfect numbers. You need a usable estimate. Calculate rough annual totals for:

- 80C total (PF + any other 80C you already do), capped at ₹1.5 lakh

- 80D total (health insurance paid), depends on who is covered

- HRA benefit (if you pay rent and get HRA), this requires rent amount + salary structure

- Home loan interest (if applicable)

If deductions are meaningful, the old regime deserves consideration. If they’re minimal, the new regime becomes more likely.

Step 3: Check One Thing People Miss – Does Your Salary Structure Even Allow HRA?

- If your salary has no HRA component, you cannot claim HRA exemption

- If you do have HRA, your rent and city category will influence the exemption

So before assuming “rent = old regime wins”, confirm: HRA exists in your salary breakup.

Step 4: Compare Both Regimes Once (Don’t Guess)

Use any reliable side-by-side calculator and enter:

- your income

- your deductions/exemptions (from Step 2)

Then compare total annual tax in both options. How to interpret results:

- If the difference is small, choose based on simplicity and monthly cash flow preference

- If the difference is clear, choose the cheaper option and move on

Step 5: Submit to HR But Don’t Over-Promise Deductions

If you choose the old regime and declare deductions:

- declare only what you can realistically provide proof for later

- avoid “wishful declarations” (they cause year-end tax shocks)

If you choose the new regime, accept that deductions like HRA/80C/80D won’t reduce your tax (for that year)

A Quick Sense Check (Use Only After You Calculate)

- If you have rent + HRA, PF, and insurance/home loan, the old regime often deserves consideration

- If you have few or no deductions, the new regime is often simpler and competitive

Closing Thoughts: Make This a Thoughtful Decision, Not a Stressful One

Choosing between the Old and New Tax Regime isn’t about finding a universally better option. It’s about choosing what fits how your salary is structured and how your money already moves.

Most regret doesn’t come from the choice itself, but from making it without understanding the impact.

Before You Submit

- Don’t copy a colleague’s choice, your salary structure is different.

- Don’t default to last year’s option, your situation may have changed.

- Don’t rush because the deadline is close, this decision affects your take-home pay for months.

If you’ve read this guide and worked through the checklist, you’re already ahead of most salaried employees.

A Note About January–March

Late declarations or TDS adjustments often show up as a sudden dip in take-home salary during the last few months of the year — even when income hasn’t changed.

That’s usually a timing issue, not a mistake.

Making a clear tax decision early helps smooth this out going forward.

If your salary dips in January–March and you’ve wondered why, this explains what’s happening and what actually helps:

→ Why Your Salary Drops in Jan–Mar (And How to Handle the Cash Flow)

Looking Ahead

Your tax regime choice isn’t permanent. Revisit it each year as your income and responsibilities change.

Do that, and tax season becomes manageable instead of stressful.