If you’ve ever compared personal loans, you’ve probably seen this situation:

- Same loan amount

- Almost the same EMI

- Same tenure

On paper, both options look identical. That’s exactly why so many expensive loan mistakes start here.

So most borrowers do what feels logical. They pick the one that approves faster or the one they saw first. Nothing about that choice feels risky. And yet, this is how many people end up paying more than they expected without ever feeling like they made a bad decision.

Because two personal loans that look the same on day one can behave very differently over the next few years.

Why This Confusion Happens So Often

Personal loans are made to feel simple.

You’re shown:

- One EMI number

- One tenure

- A monthly commitment that fits neatly into your salary

That presentation makes loans feel interchangeable. If the EMI fits your budget, the loan feels safe. What you’re not shown clearly is how the loan behaves once life moves beyond the first few months and that’s where the real differences live.

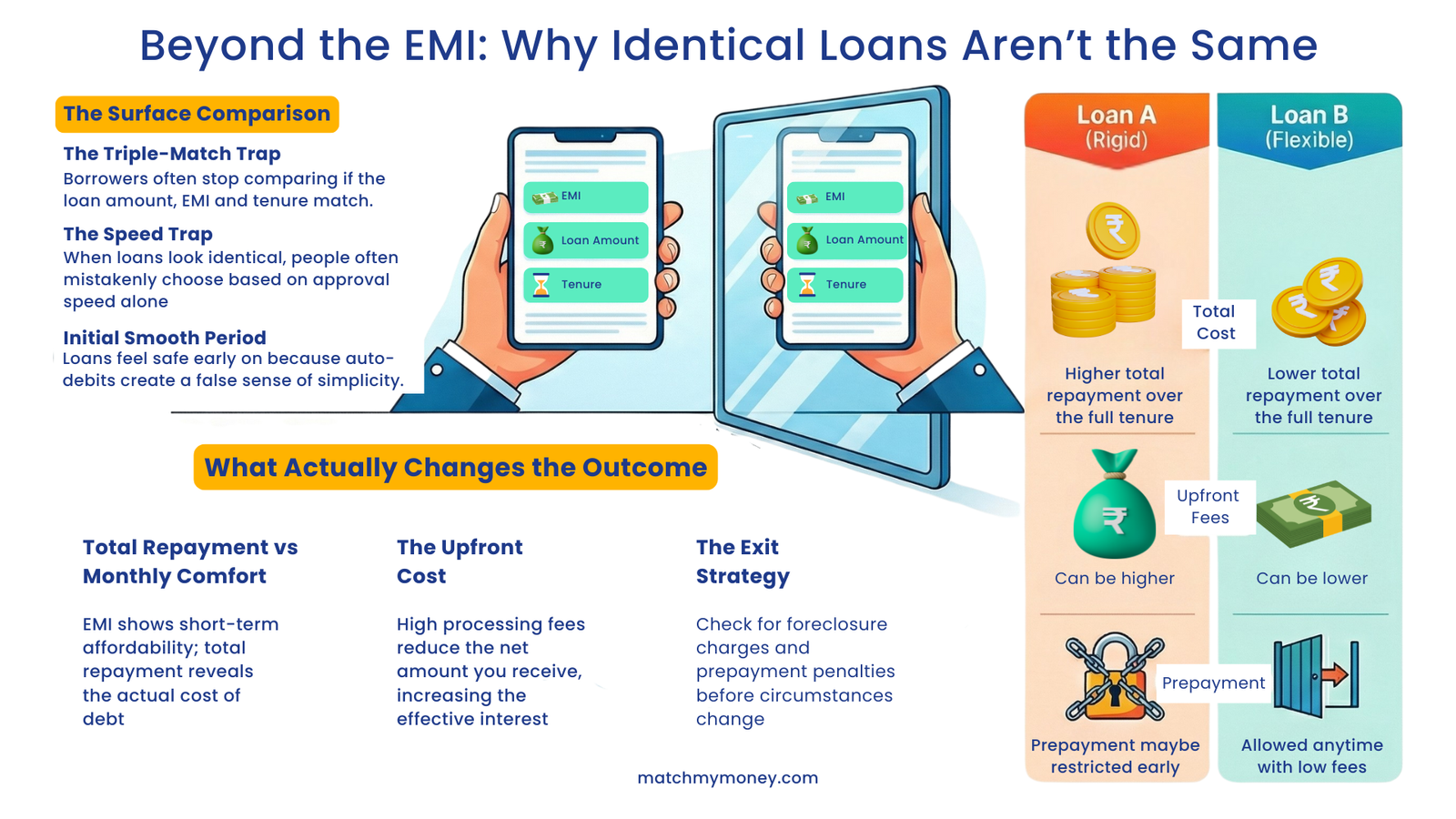

What Most People Actually Compare (And Why It’s Incomplete)

When borrowers compare personal loans, they usually stop at three things:

- Loan amount

- EMI

- Tenure

If all three match, the decision feels complete. But these numbers only describe how the loan feels today, not what it costs or how it behaves over time.

Think of it like choosing between two cars: They look the same, cost the same, and drive smoothly on day one. But maintenance, fuel efficiency, and resale value decide which one really costs more.

Personal loans work the same way.

Where the Real Differences Hide (And How They Affect You)

Let’s break down the differences that don’t show up immediately, but matter the most.

1. Interest Rate vs Total Repayment (This Is Where Money Leaks Quietly)

Two loans can have EMIs that differ by just a few hundred rupees. That feels negligible.

But over 3–5 years, even a small rate difference can mean tens of thousands of rupees extra in total repayment.

Why people miss this:

- EMI looks manageable in both cases

- The extra cost is spread quietly across months

- There’s no “shock moment”

By the time the loan ends, one option simply costs more without ever feeling expensive.

A Takeaway for You:

Always look at total amount payable, not just EMI. EMI tells you comfort. Total repayment tells you truth.

2. Processing Fees That Don’t Show Up in EMI

Processing fees are usually dismissed as small. But here’s why they matter:

- They’re paid upfront

- They reduce the actual amount you receive

- They increase the effective cost of borrowing

Two loans with the same EMI can start with different net disbursed amounts. That means one loan costs more from day one, even before interest starts working.

Remember:

Compare EMI after accounting for processing fees. If two EMIs are equal but one has higher upfront charges, it’s not the same loan.

3. Prepayment Rules (Where Borrowers Feel Trapped Later)

This is one of the biggest blind spots.

Some loans:

- Allow partial prepayments easily

- Let you close early with low charges

Others:

- Restrict prepayment in the early months or first year

- Charge heavy foreclosure fees

- Penalise you for trying to exit early

If your income improves or you receive a bonus, flexibility suddenly matters a lot. But by then, the terms are already locked in.

Pro Tip:

Before choosing, check:

- When prepayment is allowed

- Whether partial prepayment is permitted

- Foreclosure charges after 12–24 months

A flexible loan ages better than a rigid one.

4. How the Loan Behaves When Life Changes

Most people choose loans assuming life will stay stable. But reality looks different:

- Salaries increase

- Expenses change

- Goals shift

A good loan adapts. A bad one resists. Two identical-looking loans can feel completely different when:

- You want to reduce tenure

- You want to increase EMI later

- You want to close early

These differences don’t show up during approval. They show up when you try to make a smart move later.

Takeaway:

Don’t just ask, “Can I afford this EMI today?”

Ask, “Will this loan let me change course later?”

Why None of This Shows Up in The First Few Months

Because personal loans are smooth at the start. Early months usually:

- Run on auto-debit

- Have predictable EMIs

- Create no friction

That’s why borrowers feel confident initially.

The problems don’t appear early. They appear mid-journey, when switching becomes expensive and options shrink.

The Speed Trap that Causes Most Bad Loan Decisions

When money is needed urgently, speed feels like safety.

Fast approval feels helpful. Comparison feels slow. And urgency quietly removes your ability to compare. But speed often replaces:

- Understanding

- Side-by-side evaluation

- Better long-term fit

This is how two similar loans quietly diverge while the borrower never realises it.

A Smarter Way to Compare Personal Loans (Without Overthinking)

You don’t need complex analysis. Before applying, just answer these four questions:

- How much will I repay in total?

- What fees am I paying upfront?

- How flexible is this loan if my income changes?

- How easy is it to close or adjust later?

Seeing these answers side by side changes decisions immediately.

If you want a simple, step-by-step way to apply this thinking in real life, this guide breaks it down clearly:

👉 How to Compare Personal Loan Offers Like a Pro

Why Comparison Works Best Before You Apply

Once you apply:

- Credit checks happen

- Options narrow

- Switching becomes harder

That’s why comparison is most powerful before commitment, not after approval. Two loans may look the same at entry. They don’t behave the same over the full journey.

The Insight Most Borrowers Miss

Personal loans don’t just differ in numbers.

They differ in:

- Cost structure

- Flexibility

- How forgiving they are over time

These differences don’t shout. They whisper. And unless you pause to compare, you won’t hear them.

If You Want the Full Picture

This article explains why similar-looking loans aren’t actually similar.

Taking a Personal Loan? Read This Once Before You Decide, a simple guide to how EMI, interest rate, and tenure actually work together.

Seeing the full picture makes comparison easier and expensive mistakes rarer.

Final Thought

Two personal loans can look identical on day one.

The difference shows up in:

- What you pay over time

- How flexible the loan feels

- How easily you can move on when life changes

The smartest borrowers don’t rush that comparison. They take one extra look and save themselves from surprises later.