A CIBIL score of 750 or higher is often considered the benchmark for getting a personal loan. It tells lenders that you’ve handled credit responsibly in the past. You’ve paid your EMIs on time, avoided major defaults, and built a solid repayment history.

So when a personal loan application is still rejected, it can feel confusing. If your credit score is strong, what went wrong?

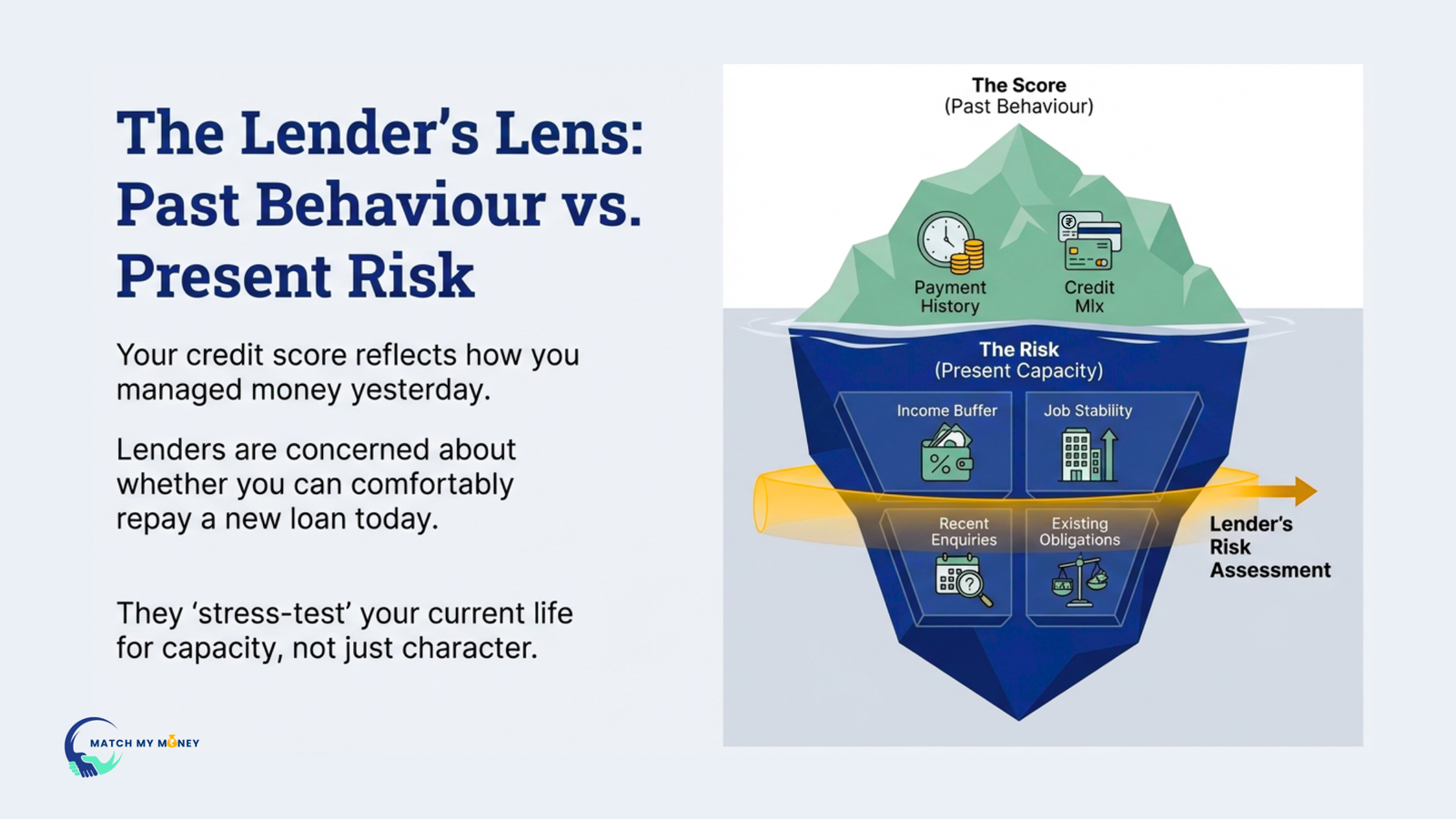

The reality is that lenders don’t approve loans based on your CIBIL score alone. While it plays an important role, it’s only one part of a much bigger picture. Your credit score reflects how you managed money in the past. Lenders, however, are more concerned about whether you can comfortably repay a new loan right now.

In this article, we’ll break down the real reasons why people with a 750+ CIBIL score still face personal loan rejections, and how you can improve your chances the smart way.

Your Income Doesn’t Support the Loan Amount

Every bank and NBFC has a minimum income requirement, but that number alone doesn’t decide approval. What lenders really evaluate is how much of your take-home salary will be left after the EMI.

Most lenders are comfortable when your total EMIs stay within 40–50% of your net monthly income. If your existing EMIs plus the new loan cross this range, the application starts to look risky, even if your CIBIL score is above 750.

For example, if you earn ₹50,000 a month and already pay ₹18,000 in EMIs, adding another ₹10,000 EMI pushes your repayment burden beyond what many lenders consider safe. On paper, your credit history is perfect. In reality, your income doesn’t leave enough buffer.

Lenders also look at how stable your income is. A fixed salary from a regular job is usually seen as more reliable than income that fluctuates month to month. This is why freelancers, self-employed professionals, and gig workers sometimes face more scrutiny, even with a strong CIBIL score.

Too Many EMIs = Low Repayment Capacity

Lenders don’t just look at whether you’ve paid EMIs on time. They look at how much breathing room your salary has after all obligations are deducted. Home loans, car loans, personal loans, credit card EMIs, everything is added up.

Internally, lenders stress-test your profile. They assume worst-case months, not best ones. Months where expenses rise, bonuses don’t come in, or unexpected costs show up. If your salary leaves very little buffer after EMIs, the risk increases sharply.

This is why even borrowers with a perfect repayment record can be rejected. A perfect repayment history doesn’t matter if your salary leaves no buffer for the next six months.

High credit card utilisation makes this worse. Large outstanding balances reduce flexibility and signal that your income is already doing a lot of heavy lifting. Even if you never miss a payment, lenders worry about how easily your finances could tip under additional stress.

Job Stability Still Matters More Than Score

Most lenders are cautious when an applicant has been in their current job for less than 6 months. Even with a good salary and credit score, a short tenure can trigger a rejection because the income hasn’t proven stable yet.

Certain situations raise additional red flags:

- A recent job change with a sharp income jump

- Employment in industries known for frequent layoffs or contract churn

- Multiple job switches within a short period

These don’t automatically mean rejection, but they do increase scrutiny.

On the other hand, some factors are seen as softer risks:

- A steady role in the same industry

- Consistent salary credits, even after a job switch

- Clear career progression rather than frequent lateral moves

If your employment history suggests predictable cash flow, approval becomes easier regardless of how high your CIBIL score is.

Errors in Your Application Can Lead to Rejection

Even with a strong CIBIL score and stable finances, applications can be rejected due to simple verification issues.

Before applying, double-check that:

- Your name, address, and date of birth match exactly across PAN, Aadhaar, bank records, and employment documents

- The income declared in the application aligns with your salary credits and payslips

- All required documents are complete, clear, and up to date

When systems can’t verify information instantly, applications often fail automated checks without manual review.

A few minutes of careful verification can prevent an otherwise avoidable rejection.

Too Many Loan Enquiries Can Hurt Your Chances

Every personal loan application triggers a hard enquiry on your credit report. One or two inquiries are normal. What lenders worry about is clustered enquiries, multiple applications within a short span.

This isn’t just about a small dip in your CIBIL score.

To lenders, repeated enquiries signal urgency. They suggest that the borrower is either being rejected elsewhere or is under financial pressure. Even with a 750+ score, this pattern can make an otherwise stable profile look risky.

Many borrowers make this mistake after their first rejection. They apply to several banks and apps, hoping something sticks. In reality, each additional application reduces confidence rather than improving odds.

From a lender’s point of view, the strongest profiles are selective, not desperate.

This is where applying smart matters more than applying widely.

Instead of sending applications everywhere, it’s better to compare options first and apply only to lenders that match your income level, job profile, and existing obligations. This reduces unnecessary enquiries and improves approval probability.

Using a comparison platform helps you do exactly that shortlist lenders before you apply, not after you get rejected.

Age, Location, and Lender Policy Filters

Most lenders have strict age limits for personal loans. If you are too young, too close to retirement, or outside their preferred age range, your application may not qualify, even with a high CIBIL score.

Location can also play a role. Certain cities, towns, or PIN codes fall outside a lender’s active service areas or risk zones. In these cases, applications are rejected automatically due to internal policies, not personal finances.

Each bank and NBFC also follows its own approval rules. Some focus on specific customer profiles, income ranges, or regions. If your profile doesn’t match their criteria, the system may decline your application without further review.

This just means that not every rejection is about your creditworthiness. Sometimes, it’s just about lender-specific policies.

While your CIBIL score is a summary of how you’ve handled credit in the past, what it doesn’t show is your current financial situation. So, while your past credit history matters, your present financial situation matters more. That decision is based on how well your present-day finances support a new loan.

Before You Apply for a Personal LoanBefore submitting another application, do a quick self-check. Most lenders are comfortable when:

If one or more of these are out of range, your chances of rejection increase even with a 750+ CIBIL score. Fixing these gaps before applying can significantly improve approval odds and help you avoid unnecessary credit enquiries. |

Don’t Rush Your Loan. Get It Right.

A high CIBIL score improves your chances, but approvals still depend on how your overall profile fits a lender’s criteria. That’s why applying blindly often leads to unnecessary rejections and repeated credit enquiries.

A smarter approach is to compare loan options first.

MatchMyMoney brings personal loan offers from multiple lending partners into one place, so you can compare details like loan amount, interest rates, tenure, and expected disbursal timelines before taking the next step. Seeing these differences upfront helps you make a more informed decision.

Choose carefully. Apply selectively. And let your CIBIL score work for you, not against you.

Start now and take a smarter step toward the right loan.