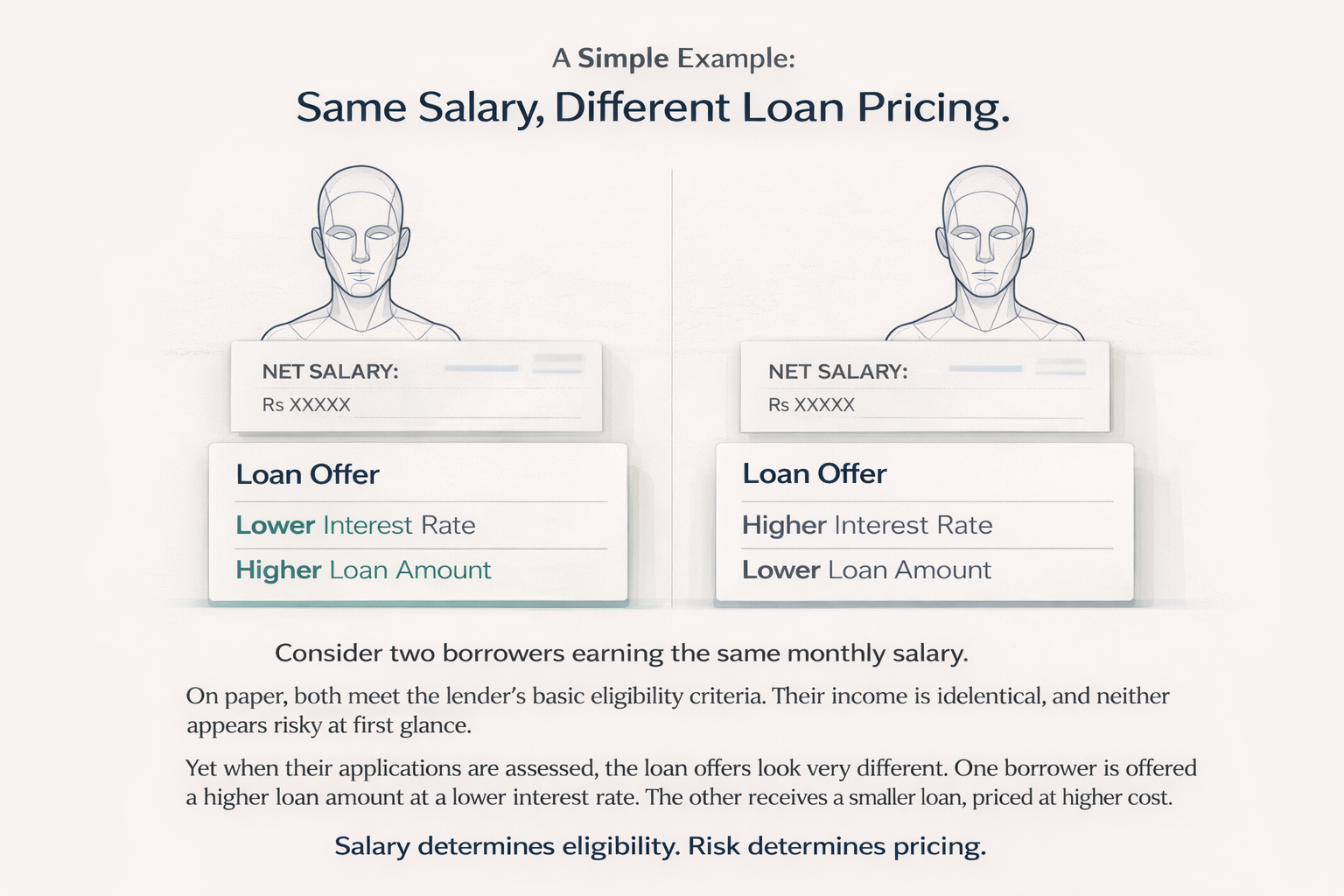

It’s common to assume that your salary decides the kind of loan offer you get. If two people earn the same amount, their loan terms should also be similar. But in reality, that’s rarely what happens.

One person might get a lower interest rate and a higher loan amount. The other might be offered a smaller loan at a higher rate, even though their monthly income looks the same on paper.

This difference often feels unfair or confusing. After all, if the salary is equal, what exactly is causing the gap?

The answer is that lenders don’t judge borrowers solely by income. Salary helps them understand whether you qualify at a basic level, but it doesn’t explain how risky or reliable you are as a borrower.

In this blog, we’ll explain why borrowers with the same salary can receive very different loan offers and what actually shapes the terms you are given.

Salary Is Only the Starting Point

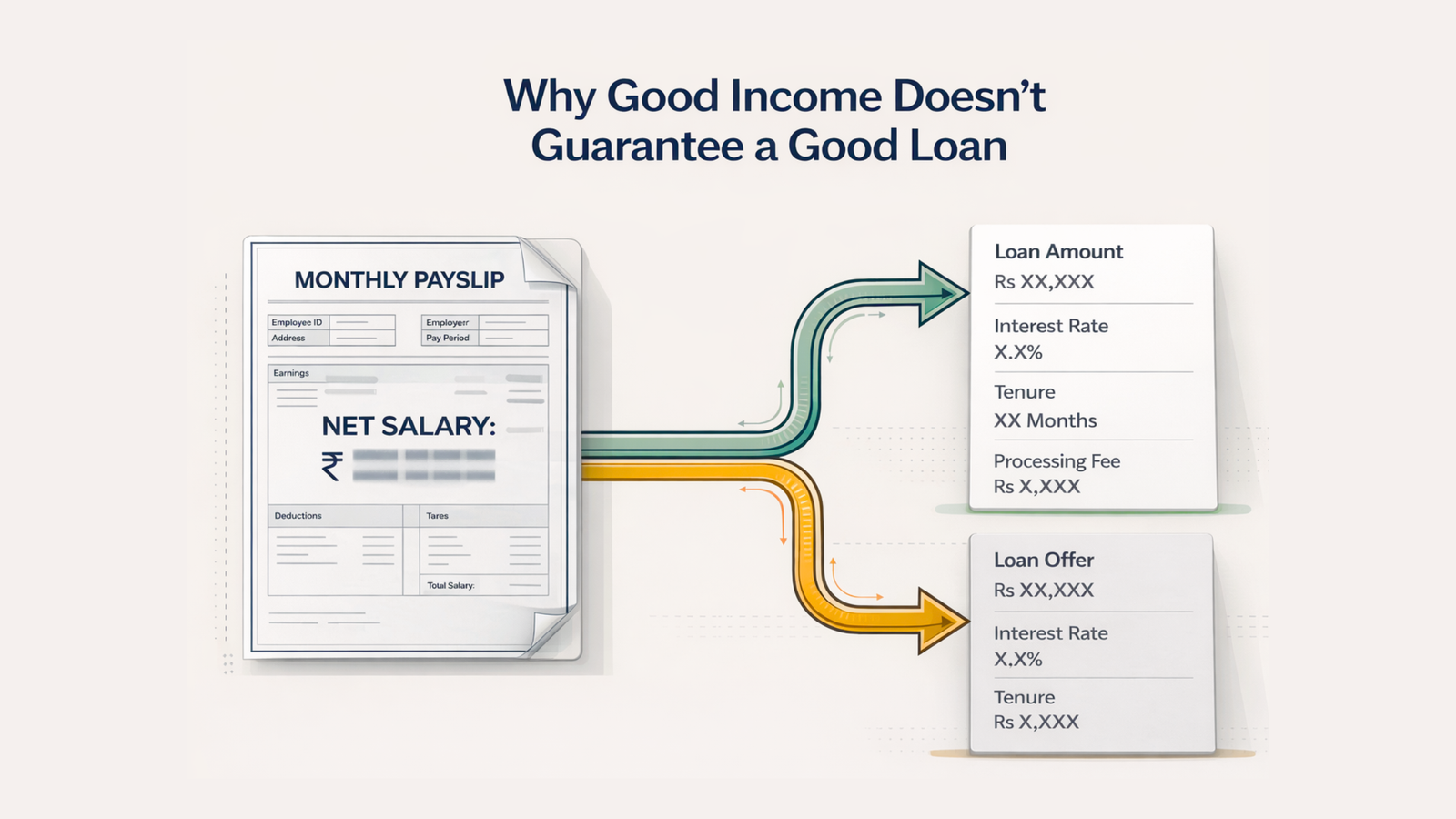

Income helps lenders understand whether you can afford a loan at all. It sets a basic limit on how much you might be eligible to borrow. But once that box is checked, lenders move on to more important questions: How predictable is your income? How much of it is already committed? And how responsibly have you handled money in the past?

This is why two people earning the same amount can still be treated very differently. One may have steady expenses, low debt, and a clean credit record. The other may be juggling multiple EMIs or have an uneven financial history. On paper, their salaries match. In reality, their risk profiles don’t.

Why Do Lenders Price Loans Based on Risk?

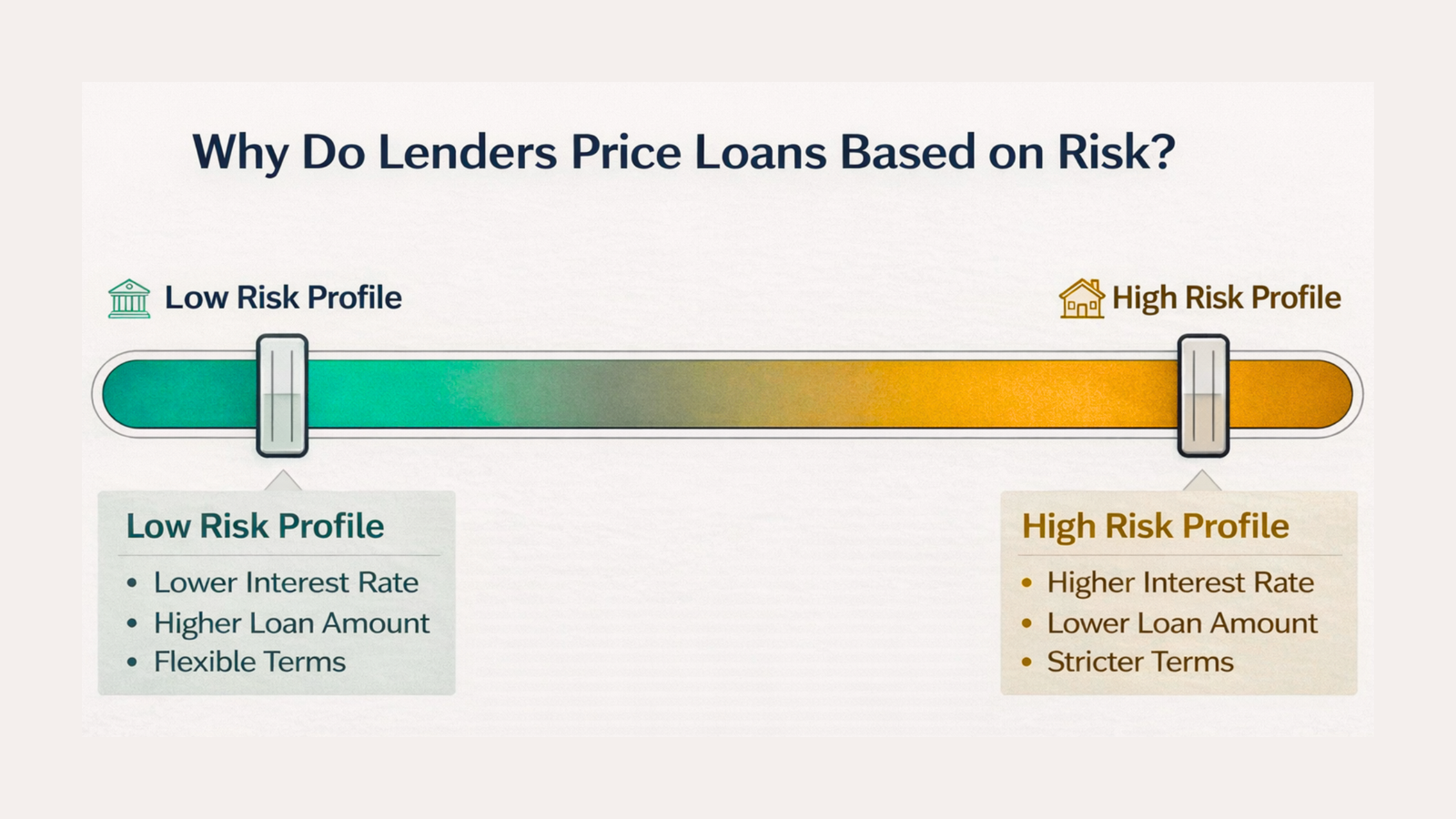

When lenders decide what interest rate and terms to offer, they don’t aim to treat everyone equally. They aim to price loans based on risk.

This is called risk-based pricing. A borrower who looks safer is usually offered a lower interest rate and more flexible terms. A borrower who looks riskier is charged more, even if their salary is the same.

Risk is assessed based on all the factors discussed so far: credit history, existing EMIs, job stability, and spending behaviour. Each of these adds to or reduces confidence in your ability to repay on time.

What many borrowers don’t realise is how sharply these factors are weighted. Small differences, like one extra active loan, a few delayed payments in the past, or higher monthly commitments, can push a borrower into a different risk bracket altogether.

Once that happens, the change is not marginal. Interest rates, approved loan amounts, and even tenure options can shift noticeably, even though the salary remains unchanged.

How Banks and NBFCs Decide Your Loan Terms

Here’s what banks and NBFCs actually look at when deciding your loan offer.

Credit History

Two people can earn the same salary and still look very different to a lender. The main reason is their credit history.

Your credit record shows how you have handled money over time. It includes whether you paid your EMIs on time, how often you used credit, and how long you have been borrowing. Someone who has always paid on time and kept their credit use low appears more reliable than someone who missed payments or used most of their credit limit.

Lenders also look at how long your credit history is. A longer record gives them more information to work with. If one borrower has years of consistent repayments and the other has only recently started using credit, their risk levels will not be considered the same.

Even small differences can matter. A few late payments in the past or a habit of maxing out credit cards can push a borrower into a higher risk category, which usually means a higher interest rate or stricter terms.

Existing Loans and EMIs

Lenders look beyond your salary to see how much of it is already committed to EMIs. A borrower with fewer fixed obligations has more flexibility each month, while someone managing multiple loans has less room to absorb surprises. Even with a perfect repayment record, lower buffers means higher perceived risk when expenses rise or income changes.

Lenders effectively test your income for stress. The higher your fixed EMIs, the less flexibility you have if expenses increase or income is interrupted. Profiles with limited buffers are priced more cautiously, even when repayment history is perfect.

Job Profile and Income Stability

Not all income is viewed the same way by lenders, even if the amount is identical.

Someone with a permanent role in a stable industry is usually seen as a safer borrower than someone working on short-term contracts or in a field where income can change suddenly. Lenders want to know how likely it is that your salary will continue without interruption.

They also look at how long you have been with your current employer. Frequent job changes or recent switches can make your income appear less predictable, even if your pay is good. Employment gaps can raise similar concerns.

Spending and Banking Behaviour

Lenders also pay attention to how you manage your bank account.

This includes things like how often your balance drops close to zero, whether your account goes into overdraft, and how regularly your salary is credited. A pattern of frequent low balances or bounced payments can signal poor money management, even if your income is good.

They also notice spending habits. If a large share of your income is spent immediately after payday, it may suggest limited savings or a small financial cushion. On the other hand, someone who maintains a stable balance and shows controlled spending looks more dependable.

Age, Location, and Lender Policy

Sometimes, the difference in loan offers has less to do with you and more to do with the lender’s internal rules.

Age plays a role in how long a lender is willing to give you to repay a loan. A younger borrower may be offered a longer tenure, while someone closer to retirement may be given shorter options or higher rates because there is less earning time left.

Location can also affect how lenders assess risk. Borrowers in large cities often have access to more lending options and competitive rates. In smaller towns or certain PIN codes, lenders may apply stricter criteria or offer fewer choices.

Each bank and NBFC also has its own policies. Some focus more on salaried professionals, while others are more comfortable with self-employed borrowers. Some prefer certain industries or income ranges.

Your Salary Is the Same. Your Options Aren’t.

Comparing options helps you spot where interest rates are lower, charges are fairer, and repayment terms better suit your cash flow. It also shows you which lenders are more comfortable with your income type and borrowing history.

MatchMyMoney brings personal loan options together in one place so you can compare them clearly instead of guessing. You can review key details side by side and choose a loan that aligns with your financial situation, not just your salary.

When you understand how your profile is priced, you can borrow with more control.

Start comparing now, choose with confidence later.