(A practical guide for working professionals in India)

Most of us don’t think about our credit score until the day we actually need a loan.

Maybe the salary got delayed.

Maybe a medical bill popped up.

Maybe you just need to make it through the month.

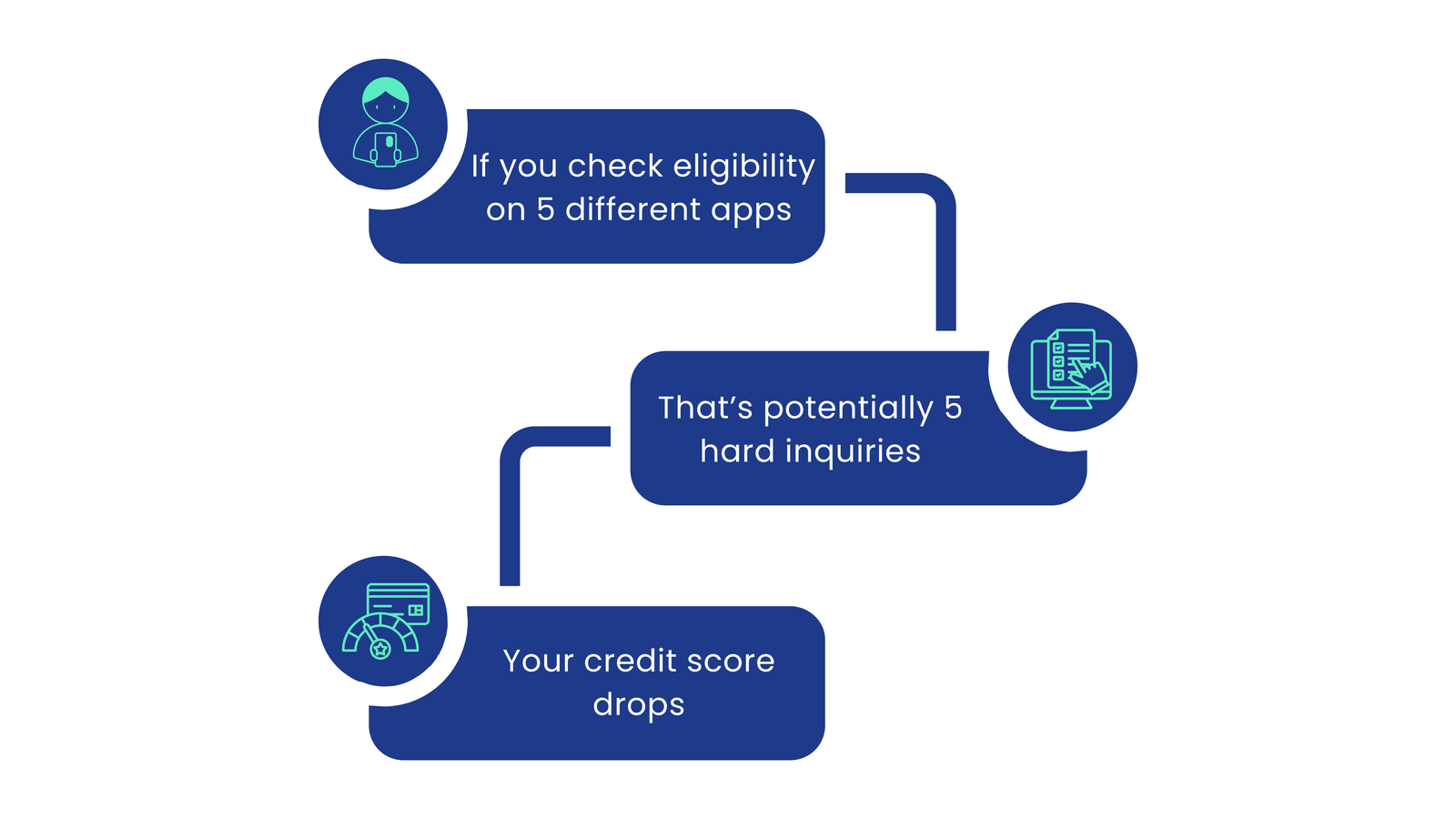

So you open a few loan apps, try checking your eligibility… and suddenly your CIBIL score dips.

“But I didn’t even take a loan, why did my score go down?”

This happens far more often than people realise.

Here’s a clean, simple explanation and the safest way to check your loan eligibility without harming your CIBIL score at all.

Read: How to Choose the Best Personal Loan in India

First, Understand What Actually Harms Your Score

Before you click on any “Check Eligibility” button, it helps to know what’s actually happening behind the scenes.

Many working professionals have borderline credit scores. In fact, a large share of Indians fall in the 500–600 CIBIL range, where even small dips can affect approval chances. This makes it even more important to be mindful of how lenders check your profile.

There are two types of checks lenders run:

Hard Inquiry

This is when a lender pulls your full credit report to decide whether to approve your loan.

Every hard inquiry lowers your score a little.

Soft Inquiry

This is a basic profile check that does not affect your credit score.

The tricky part?

Most banks and loan apps don’t clearly say which check they’re running. Many forms look like a simple “eligibility check,” but trigger a hard inquiry once you submit your details and that’s where most people get caught off guard.

2. The Real Reason Your Score Drops While “Just Checking”

When you compare loans on your own, it usually goes like this:

- You check one app

- Then another

- Then another, hoping for a better offer

What most people don’t realise is that each app may run its own hard inquiry, even if you’re simply checking “eligibility.”

To lenders, these repeated checks signal something important: This person is actively searching for credit.

In lending, that’s considered a risk factor not because you’re doing anything wrong, but because it can indicate financial stress or urgency. As a result:

- Your CIBIL score dips

- Your approval chances drop

- And many working professionals with decent salaries still get rejected

This is why it’s so important to compare safely before applying anywhere.

Read: What is a loan comparison platform?

3. How Do You Check Eligibility Safely?

The safest method is straightforward:

Use a platform that compares lenders without triggering multiple hard checks.

When you use a comparison platform like Match My Money:

- We do not run a hard inquiry

- We do not apply to any lender on your behalf

- We only match your profile against lender criteria

- You see where you stand without impacting your CIBIL score

It’s the loan equivalent of looking at the menu before ordering and you understand your options, without committing to anything.

Only when you choose to proceed with a lender does a single hard inquiry happen which is normal and absolutely safe for your credit score.

4. Why This Method Matters for Indian Working Professionals

Most people don’t look for a personal loan when life is smooth. It’s usually during a moment of pressure:

- Salary delayed

- A sudden bill

- Month-end squeeze

- A medical or family expense

And in that urgency, it’s very easy to click on multiple apps hoping one of them will approve instantly. But that’s exactly how good credit profiles get damaged.

What you actually need in that moment is clarity, not speed:

- Will I get a loan or not?

- What amount can I realistically expect?

- What will my EMI look like?

- Which lender is the safest and simplest to deal with?

When you check your chances in one place and then apply only once, you avoid unnecessary hard checks and that one small decision protects:

- your CIBIL score,

- your approval chances, and

- your final interest rate.

5. How to Check Your Eligibility Correctly (Step-by-Step)

Here’s a simple way to get clarity without harming your CIBIL score:

Step 1: Review Your Profile Once

Keep these ready so you don’t keep re-entering details on different apps:

- Last 3–6 months’ salary credits

- PAN & Aadhaar

- Your CIBIL score range (free on CIBIL website)

- Current employer details

- Existing EMIs, if any

This helps you understand where you stand before checking anywhere.

Step 2: Compare Lenders Without Applying

Look at basics like:

- Minimum salary requirement

- CIBIL threshold

- APR (total cost), not just interest

- Processing fee

- Disbursal time

- Flexibility of repayment

When you compare these first, you understand which lenders are realistic options for your profile.

Step 3: Apply Only Once

Once you know your likely eligibility, submit your application to one lender, not five. That single hard inquiry is normal and completely safe. Your score stays healthy, and your approval chances improve.

6. When Is the Right Time to Apply?

Apply only when:

- You’ve understood your eligibility

- You’ve compared 3–5 lenders

- You’re comfortable with the EMI

- You’re not guessing or panic-clicking on apps

This keeps your credit report clean and prevents avoidable score drops, especially important if you plan to take a home loan, car loan, or big-ticket loan later.

Compare Smarter. Apply Once. Protect Your CIBIL.

If you’re someone who doesn’t want to take chances with your CIBIL, especially when you know you’ll need loans in future (car loan, home loan, wedding loan) then the safest approach is: Compare first, apply once.

At Match My Money, you can check your eligibility safely across trusted RBI-registered lenders without multiple hard checks.