Lenders don’t read bank statements to confirm income. They read them to assess stress.

The statement answers a simple but critical question: Does this person have enough financial slack to repay without disruption?

A lender is less concerned about how much you earn and more interested in:

- how quickly your balance tightens after salary credit

- whether obligations leave room at month-end

- how often short-term credit is used to manage cash flow

This is why applicants with similar salaries and credit scores often see very different outcomes.

A “lender-ready” bank statement isn’t impressive. It’s predictable.

This guide focuses on how lenders interpret patterns and what actually improves approval confidence in real underwriting decisions.

Why Bank Statements Matter More Than You Think

A bank statement is not a formality in a loan decision. It’s a behavioural record.

While income establishes eligibility, the statement determines confidence. It shows how consistently an applicant can meet obligations without relying on timing, adjustments, or short-term fixes.

This is why lenders spend more time on bank statements than most applicants realise, especially in cases that sit close to approval thresholds.

Lenders Don’t Approve Income. They Approve Behaviour.

Underwriting is not a reward for high salary. It is an assessment of repayment certainty.

Lenders want to see that regular expenses, EMIs, and lifestyle costs fit comfortably within monthly cash flows. A strong income with frequent balance pressure creates more concern than a moderate income with steady surplus.

The statement reveals whether repayment happens naturally or only with effort. That distinction matters more than headline numbers.

Why Two People With the Same Salary Get Different Outcomes

Two applicants can earn the same amount and still present very different risk profiles.

One shows controlled spending, predictable balances, and clear monthly closure. The other shows tight cycles, short-term credit use, and little margin for error.

From a lender’s perspective, these are not equal profiles.

A calm statement suggests that repayments will continue even if income timing shifts or expenses rise temporarily. A stressed statement suggests that one disruption could trigger missed payments.

Loan decisions are often decided at this margin, not by income, but by how much room an applicant has to absorb pressure.

How Lenders Actually Read a Bank Statement

Lenders do not read bank statements sequentially. They scan them for signals.

An underwriter is not adding up expenses or admiring savings discipline. They are trying to understand how fragile or resilient a borrower’s monthly cash flow really is.

This reading happens in layers.

Bank Statements Are Read Like Risk Diaries

A bank statement is treated as a compressed history of decision-making under pressure. Underwriters look for:

- how income enters the account

- how quickly it is consumed

- what happens when expenses bunch together

- how often the account needs external support to function

The focus is not on one bad transaction or one good month. It is on repeat behaviour. Patterns carry more weight than explanations.

The Question Underwriters Are Quietly Asking

Every statement is evaluated against a single concern: If something unexpected happens, does this account still work? Unexpected events could be:

- delayed salary credit

- medical or family expenses

- variable income components changing

- temporary increase in EMIs

A statement that shows buffer and routine suggests resilience. A statement that runs tight or relies on timing suggests vulnerability.

Why the Last 30–60 Days Carry Disproportionate Weight

Recent behaviour matters more than older history. Lenders assume that the most recent months reflect:

- current obligations

- current lifestyle

- current financial stress levels

A clean statement six months ago does not offset pressure seen last month. Similarly, one stable month is rarely enough to override a stressed recent pattern.

This is why lenders often ask for the last two or three statements, not to average them, but to confirm consistency.

What a “Calm” Bank Statement Actually Looks Like

A calm bank statement is not flawless. It is structurally comfortable.

Lenders are not looking for aggressive saving or unusually high balances. They are looking for evidence that your monthly financial life runs without constant correction.

Three characteristics consistently signal this.

Predictability Over Perfection

Lenders are wary of statements that look impressive but inconsistent. Large balances followed by sharp drops, sudden spending spikes, or irregular patterns create questions even when income is strong.

A calm statement shows:

- regular salary credits

- familiar expense patterns

- no dramatic swings that require explanation

Predictability tells a lender that the account holder is not improvising every month.

Monthly Slack: The Most Underrated Signal

The clearest indicator of calm is residual balance.

Underwriters look at what remains after:

- EMIs

- fixed expenses

- routine lifestyle spending

An account that reaches near-zero well before month-end signals tight cash flow. An account that consistently retains a buffer signals room to absorb stress.

Consistency Beats Spikes

Lenders prefer three steady months over one outstanding one. Irregular salary amounts, frequent narration changes, or variable credit timing reduce income certainty. Even when explained, inconsistency increases perceived risk.

A calm statement shows:

- similar salary credits month after month

- predictable debit timing

- clear monthly closure

Consistency lowers the lender’s need to second-guess.

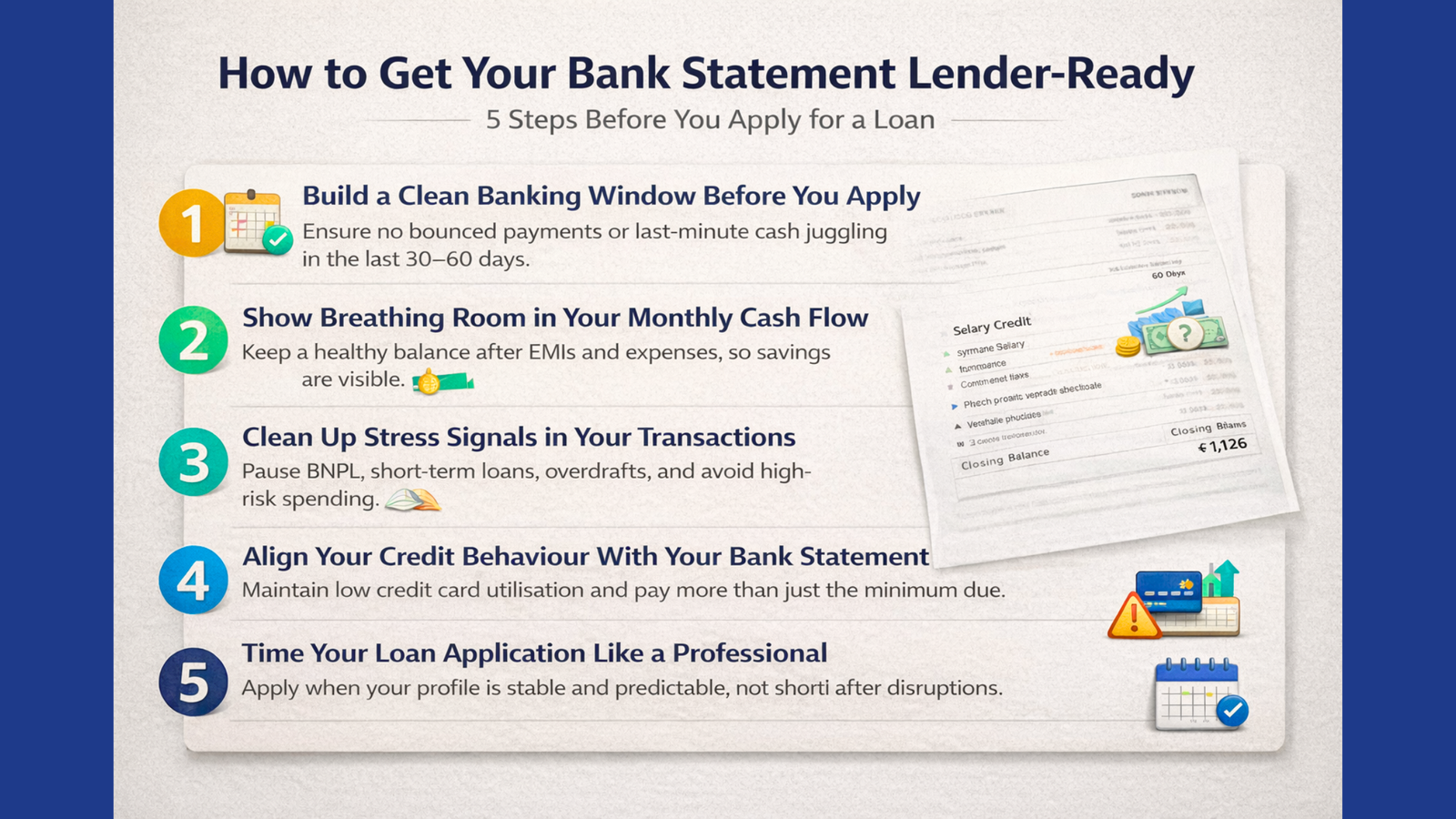

Step 1: Build a Clean Banking Window Before You Apply

The single most effective improvement you can make to your loan profile does not involve earning more or restructuring debt. It involves discipline in the weeks leading up to your application.

Lenders place disproportionate weight on recent behaviour because it reflects how your finances are functioning right now. For most personal loan decisions, the last 30–60 days carry more influence than the rest of the year.

Zero Tolerance for Bounces and Penalties

Auto-debit failures and penalty charges are treated as stress signals, regardless of amount.

A bounced utility bill or a missed subscription payment suggests that obligations are being managed tightly or reactively. From a lender’s perspective, this raises questions about how a new EMI will behave under pressure.

During the clean window:

- ensure all auto-debits are funded

- monitor small recurring payments

- avoid last-minute balance top-ups to cover debits

Even a single failure can weaken an otherwise strong profile.

Avoid “Chaotic” Transaction Clusters

Lenders notice when transactions become dense and irregular close to the application date.

Multiple rapid transfers, frequent account sweeps, or repeated small credits and debits can suggest short-term cash juggling. This does not necessarily indicate poor financial health, but it increases uncertainty.

A calm window shows:

- evenly spaced expenses

- minimal inter-account movement

- no visible cash-flow firefighting

Clarity matters more than activity.

Why Last-Minute Fixes Rarely Work

Applicants often attempt to “clean up” their statement just before applying, like moving money around, pre-paying expenses, or temporarily parking funds.

Underwriters are trained to recognise these patterns.

What builds confidence is not a sudden improvement, but continuity. Two quiet, disciplined months communicate far more than a dramatic final week.

If your recent statement shows stress, waiting to apply is often the smarter move.

Step 2: Show Breathing Room in Your Monthly Cash Flow

Lenders are not concerned with how efficiently you use every rupee. They are concerned with what happens after your obligations are met.

A bank statement that runs tight month after month suggests fragility, even when income appears sufficient. What lenders want to see is evidence that your financial life can absorb small shocks without immediately breaking.

Why Zero Balance Mid-Month Is a Red Flag

When an account consistently approaches zero before the month ends, it signals dependency on timing.

It suggests that expenses and EMIs leave little margin for error. Any delay in income or increase in costs could push the account into distress.

From a lender’s perspective, this is not about budgeting discipline. It is about repayment resilience.

An account that holds a balance through the month, even a modest one, indicates control.

Salary In, Salary Out: Why This Pattern Hurts You

Immediate withdrawals or transfers after salary credit weaken lender confidence.

This behaviour suggests that income is already pre-committed, leaving little flexibility. Even if expenses are legitimate, the pattern tells a story of tight cash flow.

Lenders prefer to see salary settle into the account, with expenses flowing out gradually. This pacing indicates that obligations are being managed, not chased.

What a Healthy Residual Balance Signals

A healthy residual balance does not need to be large. It needs to be consistent.

After EMIs and routine expenses are paid, the statement should show enough remaining to cover daily living without strain. This signals that a new EMI will sit comfortably within existing cash flows rather than competing with them.

For borderline cases, this single factor often determines the outcome.

Step 3: Clean Up Stress Signals in Your Transactions

Not all transactions are treated equally. Some patterns carry far more weight than their monetary value because they indicate how an account behaves under pressure. Lenders are trained to spot these signals quickly.

They are rarely discussed openly, but they influence decisions more than most applicants realise.

BNPL and Short-Tenure App Loans Signal Cash-Flow Strain

Buy Now, Pay Later products and short-tenure app loans are not evaluated as convenience tools. They are interpreted as gap financing.

Even when amounts are small, frequent BNPL usage suggests that regular expenses are being managed in instalments rather than absorbed comfortably. This raises concern about how an additional EMI will fit into the month.

Closing or pausing these facilities before applying materially improves perceived stability.

Overdraft and Credit-Seeking Behaviour Reduces Confidence

Occasional overdraft usage is not automatically negative. Repeated reliance is.

When a statement shows frequent overdraft utilisation or similar stopgap credit, it indicates that the account requires external support to function smoothly. Lenders read this as dependency, not flexibility.

What matters is not access to credit, but how often it is needed to stay afloat.

Speculative or High-Risk Spending Creates Unnecessary Doubt

Transactions linked to speculative activities such as gambling or high-risk trading apps are treated cautiously.

Speculative spending introduces volatility into cash flow and increases the probability of sudden losses. Even limited activity can raise questions about financial predictability.

For lenders, predictability is safety.

Step 4: Align Your Credit Behaviour With Your Bank Statement

A lender does not evaluate your bank statement and credit report in isolation. They are read together.

Inconsistencies between the two reduce confidence, even when each looks acceptable on its own. The strongest profiles show the same story across both: controlled use, timely repayment, and no dependency on revolving credit.

Credit Card Utilisation Is a Stronger Signal Than Limits

High utilisation weakens a profile more than most applicants expect.

A large outstanding balance on a high-limit card suggests ongoing reliance on credit to manage monthly expenses. From a lender’s perspective, this reduces available headroom.

Lower utilisation even on a smaller limit signals that spending is being absorbed by income, not deferred through credit.

Minimum Due Payments Signal Rotation, Not Resolution

Paying only the minimum due does not reassure lenders.

It indicates that balances are being rolled forward rather than cleared deliberately. This pattern suggests that credit is being used as a cash-flow tool, not as a convenience.

Consistently paying more than the minimum shows intent to reduce exposure, which aligns with the idea of stable repayment behaviour.

Consistency Across Salary Credits and Repayments Matters

Lenders look for alignment between income flow and repayment behaviour.

Irregular salary credits, changing narrations, or fluctuating repayment patterns reduce income certainty. Even when justified, inconsistency increases underwriting friction.

Clear, stable salary entries combined with predictable credit repayments strengthen confidence in future EMIs.

Step 5: Time Your Loan Application Like a Professional

Many rejections are not caused by weak profiles. They are caused by poor timing.

Lenders assess applications in the context of what your finances look like right now. When recent months show disruption, even a fundamentally strong profile can appear risky.

Knowing when to apply is as important as knowing how.

When Waiting Is Smarter Than Applying

There are periods when applying immediately works against you, even if eligibility criteria are met. Recent events that often reduce lender confidence include:

- a job switch or probation phase

- a heavy expense month

- a temporary increase in EMIs

- visible strain in recent balances

These do not permanently damage a profile, but they do increase short-term uncertainty. Applying during this window often leads to vague rejections with no clear explanation.

Why 30–60 Calm Days Can Change Outcomes

Lenders rely heavily on recent patterns to project future behaviour.

Two or three months of clean, predictable banking can materially improve how a profile is perceived. It demonstrates that obligations have stabilised and that cash flow has settled into a routine.

For borderline cases, this period often determines whether an application is approved or declined.

Applying When Your Profile Is “Quiet”

The strongest applications are submitted when nothing unusual stands out. Salary credits are consistent. Expenses follow a familiar rhythm. Balances show room at month-end.

A “quiet” profile requires less interpretation and fewer assumptions. In lending, fewer assumptions mean lower risk and lower risk gets approved faster.

Common Myths That Hurt Otherwise Good Profiles

Many applicants do the right things overall, yet weaken their chances by relying on assumptions that don’t match how lending decisions are actually made.

These myths are common and costly.

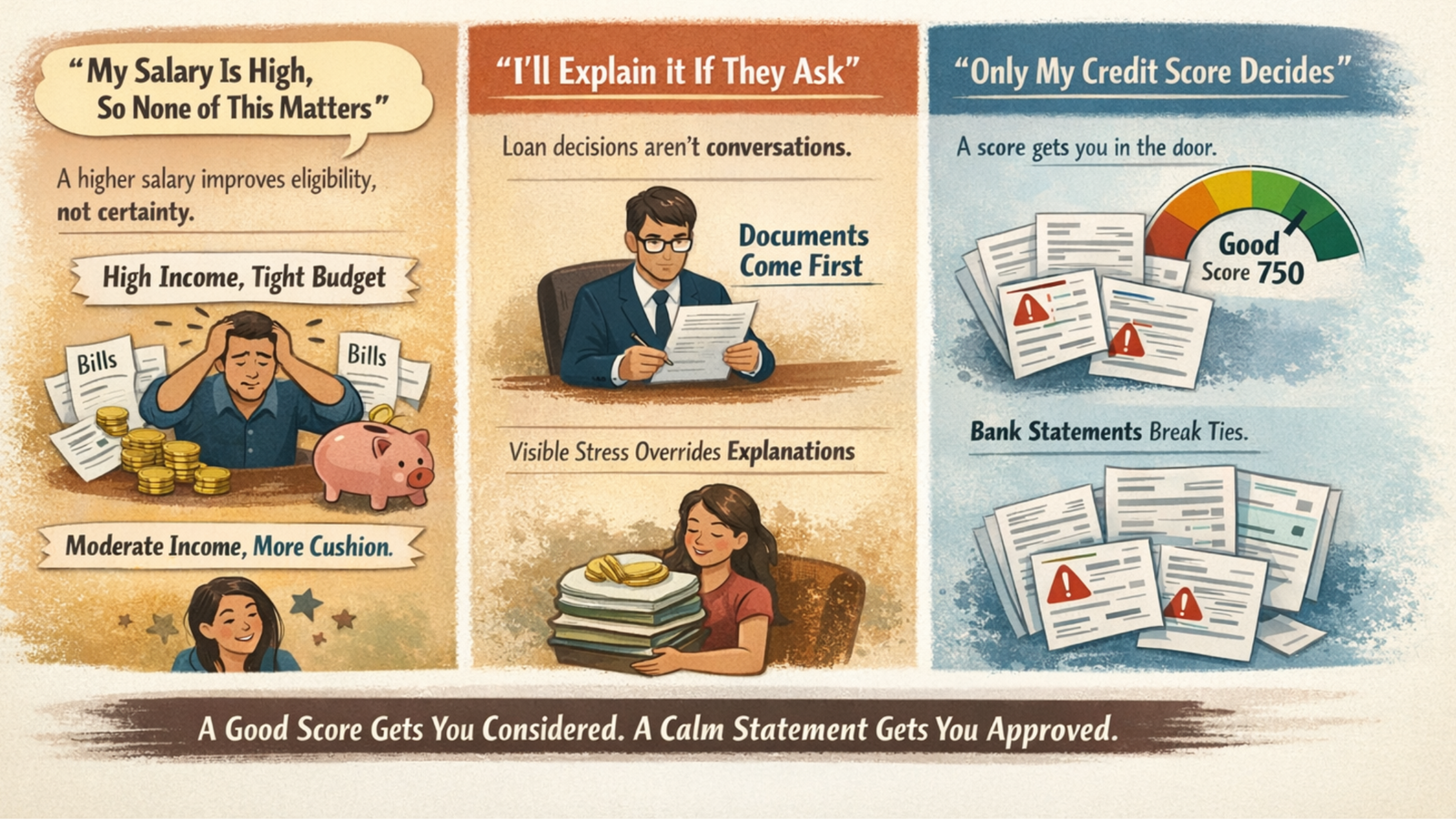

“My Salary Is High, So None of This Matters”

A higher salary improves eligibility, not certainty.

If spending patterns leave little room after obligations, lenders treat the profile as fragile. In practice, a moderate income with visible slack often feels safer than a higher income that runs tight.

“I’ll Explain It If They Ask”

Loan decisions are rarely conversational.

Most rejections happen before an explanation is requested. Underwriters work from documents, not narratives. If stress is visible in recent statements, it usually overrides explanations even reasonable ones.

Statements that require interpretation slow decisions.

Clear patterns move faster.

“Only My Credit Score Decides”

Credit scores establish baseline trust. They do not resolve uncertainty.

When multiple applicants qualify on score, bank statements are used to break ties. In these cases, behaviour and cash-flow comfort often decide the outcome.

A good score gets you considered. A calm statement gets you approved.

A Final Word Before You Apply

A lender-ready bank statement does not look impressive.

It shows that income, expenses, and repayments coexist without friction month after month.

If your statement currently shows pressure, waiting is not a setback. It is a strategy. A short period of disciplined, predictable banking often does more than chasing approvals across lenders.

Borrowing becomes easier when your finances look boring and works best when you understand your options before committing.

Match My Money brings personal loan offers from multiple lenders into one place, so you can review loan amounts, interest rates, tenure, and disbursal timelines side by.

When your bank statement is lender-ready, comparison gives you clarity. And clarity leads to better decisions.